Tired of earning 0.01% in your checking account and money market fund? For most of the last 10 years higher returns with low risk have been a bridge too far. Well, how about a safe 7.12%? The recent jump in inflation means that the current interest rate on I Bonds issued by the U.S. Treasury has been adjusted upward to 7.12%.

I Bonds are not as exciting as Bitcoin or GameStop, but you will likely sleep better at night.

Overview:

-I Bonds are officially called Series I Savings Bonds, and they offer a guarantee from the U.S. government that you can recover your original investment plus inflation increases based on the Consumer Price Index.

-I Bonds have been available since 1998, and they have offered good inflation-adjusted returns during periods from the 1990s through the mid 2000s. Investment return performance has been weak, however, over the last decade as the inflation rate remained under 2%. In cases where inflation is negative, the return is zero for that period and the principal does not decline. This actually happened in 2009 during the Great Recession when inflation was negative and the I Bond return was 0%. The recent jump in inflation has now made these investments attractive again.

-I Bonds can be considered a very competitive “parking place” for “near cash”, but you can also hold them for up to 30 years.

-I Bonds can be bought up to the last day of any month and the investor still receives the full interest payment for that month.

Inflation Adjustments: The current interest rate for I Bonds is 7.12% (for December 2021 through May 2022), and then it is adjusted every six months based on the inflation rate at that time. My Cornerstone inflation expectation is for a gradual reduction in the inflation rate, and a lower inflation rate translates into a lower I Bond return. Nevertheless, I expect an I Bond investment would significantly beat your bank rate for the next couple years.

Rates are moving up, but … The Federal Reserve announced on Wednesday that they will be raising rates, but don’t expect anything big anytime soon. The Fed’s current “Dot Plot” forecast signals three interest rate increases between June 2022 and the end of next year. The forecast also sees three additional rate increases in 2023 and three more rate increases in 2024. Based on this forecast, short-term interest rates would be around 2.25% by yearend 2024. Although short-term interest rates will slowly rise, these rate increases will rise even more slowly for your deposits in your checking and money market funds. Banks are always very quick to raise rates on loans, but they will delay raising your deposit rates as long as possible. Hey, they are in a competitive business to make a profit and meet shareholder expectations. They have also learned that you will tolerate these low deposit rates because you have had little recourse in the past. It needs to be remembered that your investment portfolio likely holds banks and you will benefit from stronger investment performance.

The maximum annual investment is $10,000 per social security number (plus up to $5,000 more if you elect to receive your federal tax refund in I bonds). If you have kids, you can set up accounts for them as well. So, if funds are available, a married couple could put in a total of $20,000 before the end of 2021 and then another $20,000 in 2022. You could do the same for kids.

You can’t get this from you Adviser/Broker: Although it would be convenient to purchase I Bonds through your existing advisory or brokerage accounts, you need to set up an account with the U.S. Treasury. I Bonds are purchased via the TreasuryDirect.gov website, and it is set up to pull cash from your checking account. There is no charge of any kind at any point. The Treasury website is very intuitive and it is designed to easily walk you through the process.

Liquidity: The I Bonds cannot be liquidated for one year after purchase. They can be redeemed between one and five years but you must forfeit 3 months of accrued interest. After five years they can be liquidated without penalty.

Taxes: You have the option of paying your federal taxes on an annual accrual or you can wait until maturity to pay the whole tax obligation. Like other U.S. Treasury securities, there is no state or local tax. If you use your income tax refund to purchase U.S. savings bonds, complete and file IRS Form 8888 with your tax return. They can also be used without taxation under some conditions for educational expenses.

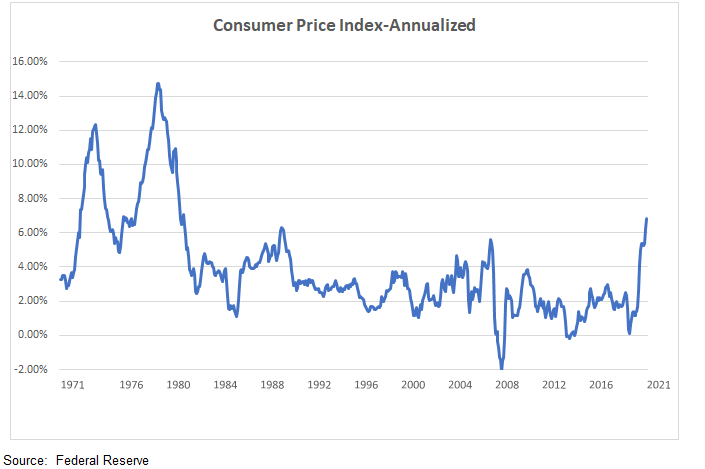

The graph below shows the current upward move in inflation and the history going back to 1971.

Jeff Johnson, CFA

December 18, 2021

Cornerstoneexists to provide educational investment information with a Christian perspective. Some posts are purely about investments (like this one), but other posts have covered stewardship and charitable giving, core values and ESG, Happiness/Money, etc. This is a unique combination, and Cornerstone continues to evolve. Your comments are always helpful and are appreciated.

2020 began with hardly a cloud in the sky. It seems like a long time ago when we gave little thought to simple things like going to work or socializing with family and friends. Going or to our kids’ or grandkids’ soccer game or shopping were routine. We knew we faced a polarizing election, but at least voters would sort it out. Most everyone had a job and the U.S. unemployment rate was at 3.5%, a 50-year low. Investors were benefitting from the longest economic expansion and the longest bull market in history, Chinese trade-war tensions were subsiding, and the 2020 outlook was promising.

Then, the lights went out and 2020 became a year like no other. COVID-19 became the dominant theme of the year, and it impacted everything. It seemed like the word “Unprecedented” was used in every other sentence.

The Shutdown Caused Many Hardships: Life came to feel surreal as normal activities ground to a halt and the economy and most other activities shut down faster than at any time in history. Lockdowns, Stay-At-Home orders, Work-From-Home and social distancing meant that many social activities, businesses, schools and churches abruptly went dark. Parents were suddenly attending to school-aged children and helping with distance learning while dealing with a precarious work environment. Unexpected impacts included shortages of toilet paper, Clorox and baking flour. Bad haircuts and motion-sensing Purell dispensers became the norm. The NBA season and the NCAA basketball tournament were early casualties. Zoom became a staple of everyday life, and “You’re muted!” became an all-to-common refrain. Who knew Domino’s Pizza would displace a nice restaurant.

With no significant pandemic experience in over a century, it was naively assumed that it would be under control by summer. Obviously, COVID-19 virus proved more formidable and forced much unexpected change. Over 10 million were unemployed by the end of March. Oatmeal consumption jumped over 200%. Liquor sales spiked in 2020 as people used it as a way to cope with mental distress. COVID fatigue set in. Isolation took its toll. People died without the presence of family and friends. Little did we know that the U.S. would grieve the loss of over 340,000 deaths over the course of the year.

Uncounted small business owners lost their life work and many displaced workers lost jobs that would not return. The number of shooting victims in New York City more than doubled in 2020, with low-income and minority communities hardest hit. As if the COVID virus wasn’t enough, the May 25 killing of George Floyd thrust America into a soul-searching reckoning related to racial injustice. Although not caused by COVID, this tragic event caused social upheaval and a deep a psychic scar. Finally, the U.S. faced a polarizing election.

Gratitude for the Real Heroes: Despite the many hardships, there came to be a recognition and profound sense of gratitude for the real heroes. The healthcare and other essential workers cared for the virus victims and kept the country functioning.

-Health care workers demonstrated incredible dedicated service despite personal danger and sacrifice as they risked their lives to save others.

-Everyday workers delivered packages and stocked shelves.

-Medical supply people provided masks, car companies produced ventilators and Clorox disinfectant production was stepped up.

-Scientists and researchers raced against time to develop treatments and vaccines.

-And finally, there were uncounted and often un-noticed acts of helping and compassion by everyday people who helped meet needs wherever possible.

These examples showed courage and persistence in the face of adversity and long hours, and they are a true inspiration. The sacrifices add up to something much bigger than is readily evident and help to comprehend the meaning of who and what is really essential.

Charitable Contributions: Although charitable giving typically declines during economic crises, numerous reports show that people actually increased their giving.

Meals on Wheels, food banks and health-related charities saw increased giving during the pandemic, as Americans opened not only their hearts but also their checkbooks. There was also a big upward shift in indirect aid. As people became more aware of the needs in their community, there was help for vulnerable neighbors and support for local businesses through the downturn.

Expressions of Basic Humanity and the Human Spirit: A common refrain has been that we are all in this together. This hardship brought out many unique expressions of solidarity and resolve. A few examples:

-People across the country cheered healthcare workers and COVID-19 survivors.

-Parades of police and car caravans celebrated birthdays and other significant events.

-Minnesota landmarks were lit in purple to honor frontline workers battling the pandemic.

-Singing from balconies and other social distanced places battled the isolation: Boston residents belted out “Lean On Me” and Chicago metro area residents responded by singing the National Anthem and “We are the Champions.”

-These events went viral on social media and helped many others to cope.

COVID-19 tested us. We didn’t always act in the noblest ways. We’re all susceptible to COVID fatigue. There were certainly situations where social distancing was ignored and super spreader events caused more cases, hospitalizations and deaths. Nevertheless, we don’t want to forget the inspirational displays of goodness and basic humanity that helped lift us all up.

Vaccines-The Beginning of the end: The word “Unprecedented” certainly applies to COVID-19 vaccine development as drug companies created a vaccine against a novel pathogen within a year of its discovery, the fastest ever. The shortest timeline previously was for the Mumps vaccine, which took four years according to the Washington Post. Not everyone gets a chance to save the world, but dedicated individuals worked relentlessly to end this pernicious virus. The work by Pfizer, Moderna and many others represents a testament to scientific genius, the spirit of invention, persistence and a commitment to a higher cause. There is also a bright spot related to this research because the Messenger RNA used by Pfizer and Moderna may be used for future therapeutics to target other diseases, including cancer.

These vaccines are truly a game changer. We can only wonder what it would be like and how we would feel if these vaccines development time took two or three years.

Return to Normal?: As the COVID-19 ordeal ends there is a natural desire to return to normal. As the isolation gradually winds down, how quickly will people feel comfortable again seeing family and friends, taking vacations and going back to baseball and football games? The reality is that we aren’t going all the way back and some changes will be permanent. It has become a cliché to state that we have experienced 10 years of change in one year. But the pandemic has accelerated structural changes long in the making. Some businesses will not return and some jobs have been lost forever. There is deep uncertainty about how consumer and office-worker behavior might have changed. There is a huge hangover of debt. Education is likely to see many permanent changes. What will our churches be like, and who will come back? Adversity causes changes, and how will people react? COVID-19 forced us to be more resilient and self-reliant. As we think of the lessons learned and our reshaped priorities, hopefully the changes will help us be more aware, patient, deeper, compassionate and thankful.

MARKET REACTION, PERFORMANCE & OUTLOOK

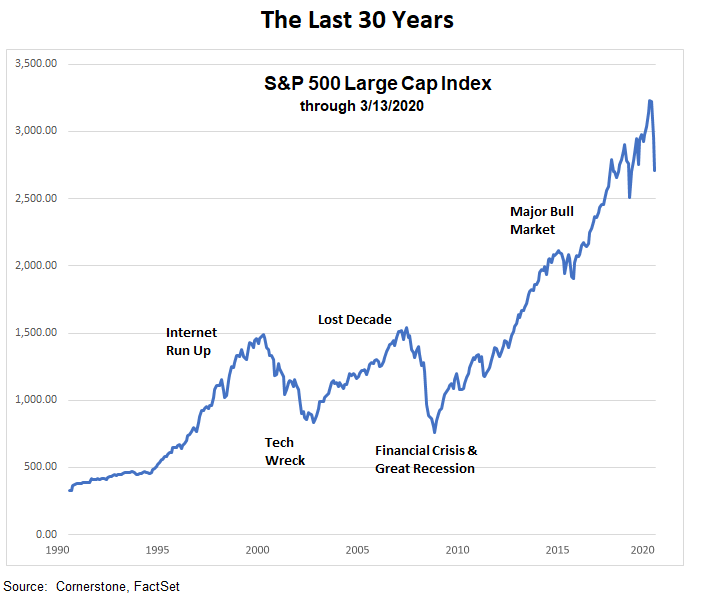

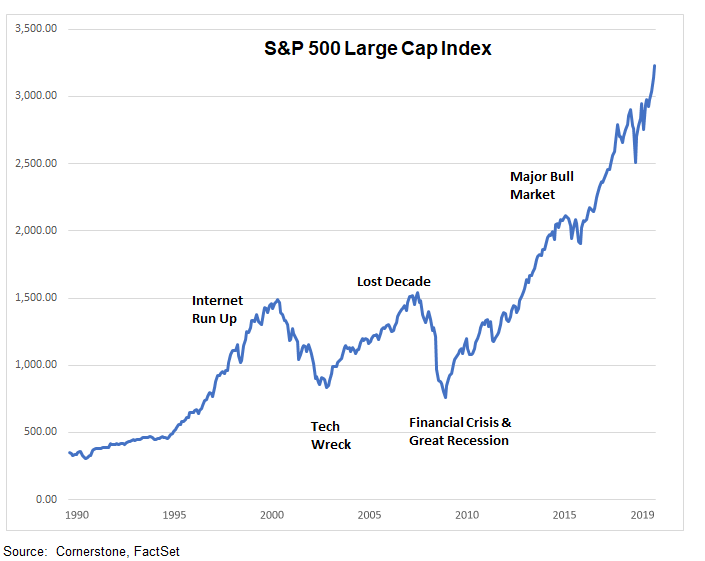

Healthcare factors aren’t typically big market drivers, but COVID-19 dominated the markets in 2020. While 2020 was volatile, it is helpful to examine the year in a broader context. The graph below shows the longest bull market in history from March 2009 through February 2020. It also shows more protracted historic bear markets that often last far longer than the recent short downturn in 2020. Although accurate short-term projections are difficult, history gives a longer perspective and says it would not be prudent to extrapolate the recent market strength forward for the next ten years.

As shown below, investors benefitted from a record long 11-year bull market. This time period was accompanied by a record long 10 ½ year economic expansion. But both streaks ended in February as COVID-19 abruptly shut down the economy. Since there was no good pandemic precedent, the market panicked with the fastest decline in history into a bear market with waves of indiscriminate selling.

Both the Federal Reserve and Congress, benefitting from what was learned from the 2008/2009 Great Recession, reacted in record time with extraordinary monetary and fiscal stimulus. The market, recognizing this unprecedented stimulus, reacted with the fastest bull market recovery in history. The whiplash in the first half of 2020 produced the most extreme quarterly performance variance since the 1930s.

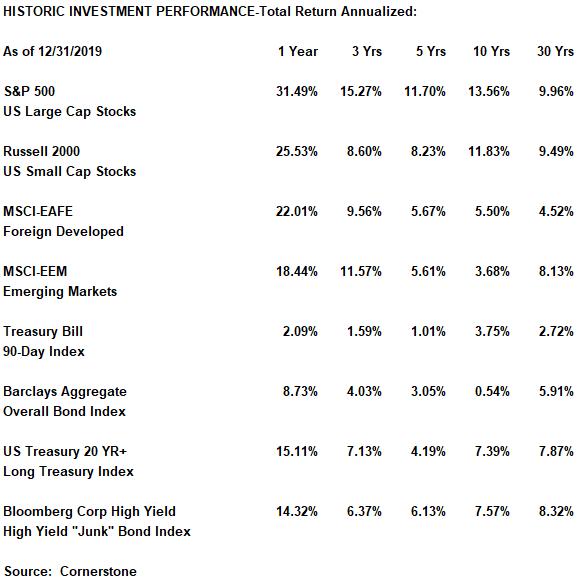

The table below provides additional perspective:

-2020 performance was generally well above historic norms.

-Volatility as measured by Standard Deviation was also high compared to the longer-term ten-year average.

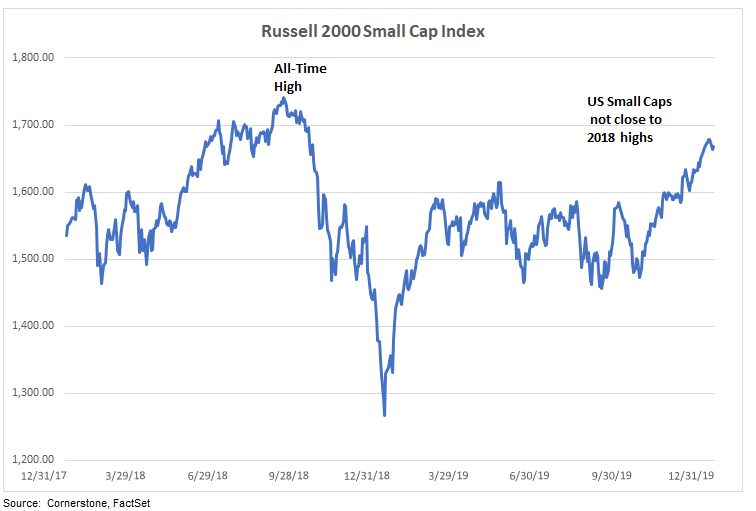

-Small cap stocks and emerging markets are particularly volatile.

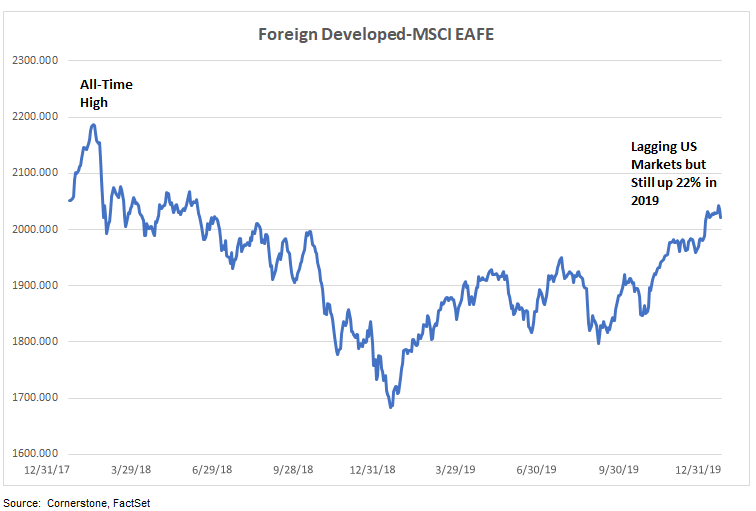

-Foreign developed and emerging markets stocks have been laggards over the last ten years.

-Long maturity U.S. Treasury bonds had extraordinary performance as interest rates declined and bond prices jumped upward (more below).

The observations from the table above provide context and perspective related to expectations for the future. One notable point is that recent performance is a poor forecast for the future. Listed below is additional information related to market expectations.

Consensus Economic Outlook:

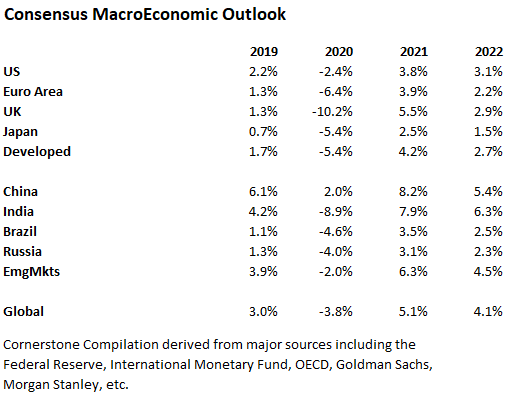

There is a difference between the economy and the stock market, and the two do not move together in lockstep. Nevertheless, the economy is a major driver of corporate profits, and corporate profits are a clear driver of the stock market. The COVID-19 virus caused a global economic recession in 2020. China and Taiwan were the only major economies to achieve positive 2020 economic growth. The recession caused a significant reduction in 2020 corporate profits and contributed to the sharp market decline in March. Consensus expectations show a significant 2021 recovery and this should help increase corporate profits and help support the market.

There are a number of reasons to support the rationale for a strong 2021 economic recovery. The rapid development of vaccines gives relief to lockdowns and shutdowns and a resumption of more normal growth. There is also a fair amount of pent-up savings and demand, and consumers are likely itching to spend some of it. It is encouraging that forecasts are being revised upward, and these positive revisions are a positive indicator. It is noteworthy that many forecasts see a rising level of inflation. Inflation has been very low over the past decade, but massive government stimulus, improving economic growth and widening government budget deficits are reasons to push inflation higher. If inflation increases, it typically doesn’t hurt stocks too much unless inflation gets up to higher levels. Higher inflation will crush long-maturity bonds, however. While these forecasts focus on the vaccines and on hefty stimulus, domestic politics and geopolitical issues continue to be potential wildcard factors. It needs to be said that economic forecasts are subject to a wide range of outcomes.

Wall Street Targets:

Wall Street has long provided price and earnings targets for the upcoming year. History shows that these expectations may not be accurate, but they do show what is priced into the market. If there are no big surprises (like the 2020 coronavirus), then these targets provide perspective and can be helpful.

A summary of the top 14 Wall Street firms compiled by CNBC shows the following:

A few comments regarding these targets:

-Central bank stimulus and COVID-19 recovery are seen as major drivers.

-The recent uptick in mergers & acquisitions is seen as continuing in 2021.

-They all show the market moving up in 2021. When everyone sees upside, much of the optimism may already be priced in and the stage could be set for a decline.

-All show lofty Price/Earnings ratios that show valuation levels well above historic levels.

Valuation:

Equity markets are expensive by most valuation metrics. The S&P 500 consensus Price/Earnings ratio for the next/forward twelve months is a common valuation measure and is listed below:

At a cursory level, it looks like the market is nearly as expensive as the late 90s internet frenzy, and you have to wonder if we are “Partying like its 1999.” Many remember how that ended. There are a couple of major differences, however, between 1999 and 2020. The 10-year U.S. Treasury bond yield was over 6% in 1999, and now it is at 0.9%. In addition, many technology companies in 1999 were young and had minimal earnings, and today’s leaders have dominant business models. (Like Microsoft, Google, Amazon, etc.)

Although valuation levels aren’t quite as stretched as in late 1999, it is still sobering to remember that the tech-heavy Nasdaq fell 78% from March 2000 to October 2002.

Market bulls acknowledge high current valuation multiples, but see equities delivering decent relative returns versus even more expensive bonds. They believe that markets look less expensive when juxtaposed on a relative basis against current low interest rates and a low inflation environment. While conceding high valuation levels, they believe equities will grow quickly and catch up to their high valuation levels.

Market bears point to the extraordinary monetary accommodation around the world driven by central bankers dealing with the virus-induced slowdown. This stimulus has made all assets expensive, and results in low forward returns for both stocks and bonds.

It seems clear that the market has pulled forward some post-vaccine economic growth into current valuations and it will take time for the U.S. to grow its way into these valuation levels. Central bank monetary stimulus has also made all assets expensive as nearly-free money distorts valuation levels. It also seems reasonable that when equities are adjusted for low interest rates, valuations aren’t quite as extreme. This is especially true given the fact that U.S. Treasury bondholders are currently receiving negative inflation-adjusted real rates of return due to low nominal interest rates.

History shows that Valuation levels are not a good predictor of short-term returns, but they are a good predictor of longer-term returns. Consequently, the current high valuation levels could persist for some time. There are market pundits predicting both an imminent bear market and a sustained bull market, but it would be a fool’s errand to confidently predict either. Regardless, current valuation levels and low interest rates point to below-trend investment returns on a longer-term basis. While returns for stocks could be lower over the next decade, they should still perform better than longer-maturity bonds.

What To Do Now:

The markets have generated big returns in 2020, and also since 2009, and it is easy to be lulled into a false sense of overconfidence. The big gains by year-end 2020 help us forget the precipitous decline in March. But markets run on fear and greed and the euphoric emotion can plummet once again into volatile, undisciplined selling. Here are some factors to consider:

-Don’t let big up or down market moves change your investment objective. Big upside market moves make us forget the pain of down markets and to overestimate our tolerance for downside risk. This could cause additional buying of an expensive market. Similarly, big down markets cause us to abandon all hope and to get too conservative and to sell at the bottom.

-Rebalance. At a high level, rebalancing involves trimming the weights of the biggest gainers (because they have grown too big compared to your strategic weight) and buying the laggards (which have become underweight). To take an extreme example, if you own Tesla-TSLA (up over 700% in 2020), then the stock and the large growth asset class are too big and should be trimmed back. The cash proceeds from the sale should be put into the cheaper underweight assets. If you are a self-directed Do-It-Yourself (DIY) investor, then you need to rebalance your portfolio. If you have an adviser, then ask them about rebalancing.

-From a tactical standpoint, Small Cap stocks and Emerging Markets have trailed in recent years and look most attractive.

-Avoid FOMO (the fear of missing out). Do your own thinking. (See below)

-Stocks that are up the most are excellent candidates for charitable giving. This is a way to help achieve a rebalanced portfolio. A key Cornerstone objective is to encourage charitable giving. See Charitable Contributions

-Avoid long-maturity bonds. If inflation heats up, these bonds will perform badly.

-Don’t make plans for 10% future equity returns. Current high valuation levels indicate that 6% equity returns are more reasonable for financial planning and retirement expectations.

More Detail and Red flags Below:

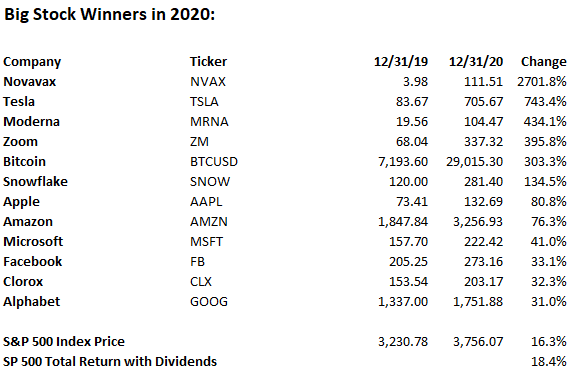

BIG STOCK GAINS IN 2020:

Investors should utilize funds unless there is sufficient time and experience to research individual securities. Even then, most investors would achieve greater returns with an index fund than picking stocks. Nevertheless, it is interesting to review some high performing and high-profile stocks as listed below:

(Sorted by 2020 returns)

Some Comments:

-The big winner was Novavax, a biotech company trading on Nasdaq that is in late-stage trials with a COVID-19 vaccine. If the vaccine gets approved, the price will be justified. Otherwise, it might return to single digits.

– Tesla is noteworthy. Tesla is the sixth-largest company in the S&P 500 but it is not profitable without regulatory emissions credits. Tesla’s market value is currently 2 times the combined value of Ford, GM and Toyota. Elon Musk is a true visionary, but the valuation looks very stretched.

-Moderna is up based on their successful COVID-19 vaccine. Few knew of Zoom before the pandemic hit, but Zoom kept us going through all the isolation.

-The S&P 500 market value is dominated by five big tech stocks: Alphabet/Google, Amazon, Apple, Facebook and Microsoft. These five stocks have significantly outperformed in the past. You might characterize the S&P 500 as the Big 5 and the little 495. The Big 5 outperformance may continue for a while but it is not likely to persist in the longer term. A diversified portfolio has stood the test of time, and an overconcentration in these stocks poses longer-term performance risks.

It may be tempting to invest in a few potential high-flyers to boost your retirement account. For example, if you bought $1,000 worth of Amazon when it came public in May 1997, it would have grown to $2,175,000 by year-end 2020. What’s not to like? For every Amazon, however, there are hundreds of losers like Pets.com and TheGlobe.com. TheGlobe.com had the distinction of spiking over 10x during its first day of trading, but its business model is long gone.

The reality is that it is difficult to find many of the big winners before they make their big moves. Most of the big 2020 stocks benefitted from COVID-19, and no one saw the virus risk at the beginning of the year. At this point it is difficult to identify the 2021 market drivers.

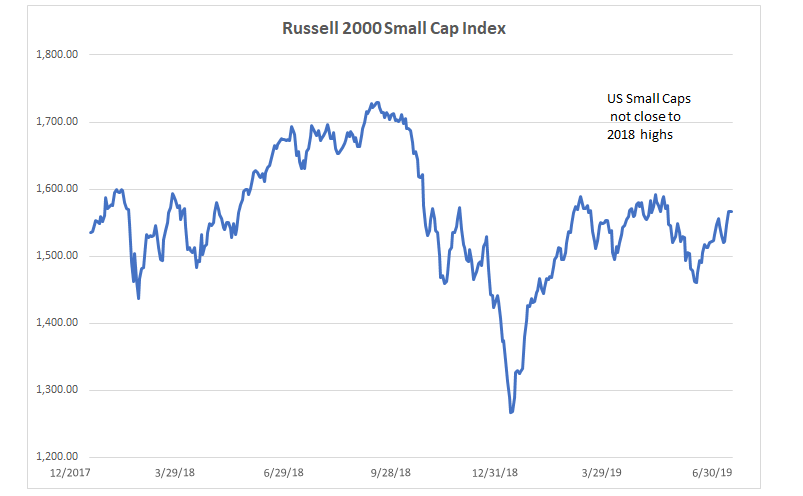

Small Cap Stocks:

Small cap stocks have outperformed large cap stocks historically, although they have been laggards over the last 10 years. Small caps as measured by the Russell 2000 index trailed large caps in 2020 until the fourth quarter.

Although small caps are more volatile, they are important in a portfolio’s overall asset allocation plan. Small caps are expected to offer significant forward growth because their greater operating leverage allows profits to grow faster in an expanding economy. Small caps have been under-owned and should benefit from increased investor interest.

Foreign Stocks:

International stocks outperformed in the 1970s, 1980s, and the 2000s, but have trailed the S&P 500 since the 2008/2009 Great Recession. International stocks are cheaper than U.S. stocks, and especially U.S. large cap growth stocks, and should benefit from investors seeking cheaper valuation levels.

Emerging Market Stocks:

Emerging Mkts: Emerging market stocks are another asset class that has trailed in recent years, but has provided a nice rebound in Q4. Emerging market stocks are more volatile but offer better growth prospects than developed markets based on a younger population and a growing middle class. China is a large component of emerging markets and it offers significant growth potential. Emerging markets benefit from a weaker dollar, they are cheaper than developed markets, they offer diversification benefits and they look poised for good longer-term performance.

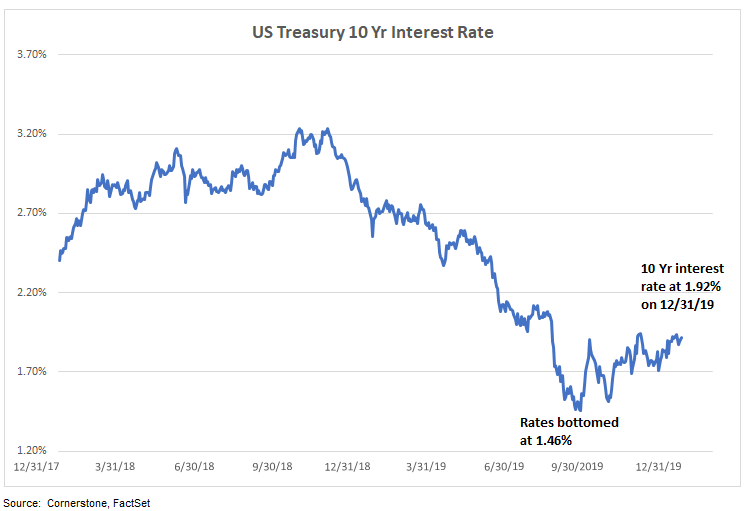

Historic Interest Rates:

Interest rates have been trending lower since the early 1980s. The 10-year U.S. Treasury bond interest rate peaked at 15.82% in September 1981 as the U.S. battled double-digit inflation. As inflation subsided, rates have trended lower. Interestingly, forecasters, including the US Federal Reserve, have consistently projected rising rates. Historic long-term bond total return performance has been high due to bond price increases as rates declined. With interest rates at current low levels, there is little potential for additional bond price gains. Instead, any increase in yields will negatively impact bond prices and will be a drag on total return performance. If inflation picks up faster than expected, then longer-maturity bonds will experience significant negative performance.

Interest Rates in 2020:

The 10-year US Treasury bond began 2020 with a 1.92% yield. As the COVID-19 pandemic spooked markets, the 10-year treasury yield briefly plunged below 0.5%, on March 9 due to recession fears. The yield then spiked upward based on a safe haven flight-to-quality trade. As vaccines allow for increased economic activity, rates have risen to 0.92% at yearend. At this time, real yields (nominal yield net inflation) are negative. Fed policy is to keep short-term rates like 90-day Treasury Bills pinned near zero through 2023. With this low interest rate backdrop, short bonds will earn very little return and longer maturity bonds may have negative returns as interest rates eventually normalize and bond prices decline.

Historic US Dollar:

The U.S. dollar peaked after Fed Chair Paul Volcker and President Reagan broke the back of double-digit inflation with high interest rates in the early 1980s. The dollar rose again between 1997 and 2002 as Germany assumed high costs of reunifications with East Germany and as Europe implemented austerity plans and increased taxes.

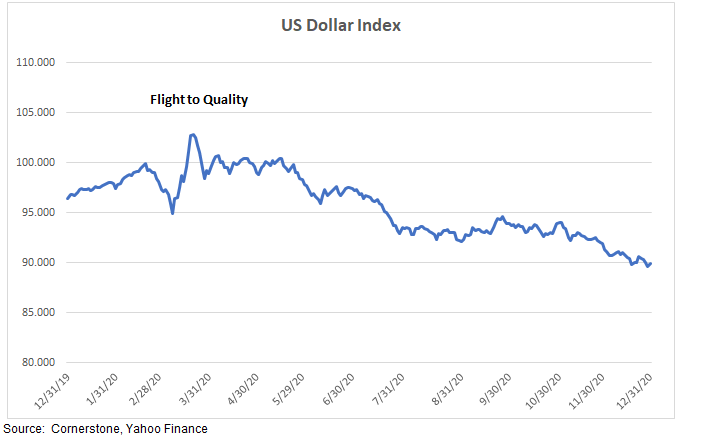

US Dollar in 2020:

The dollar was trending up in early 2020 until markets panicked and interest rates fell over recession fears from the pandemic. The dollar then blipped up in late March as traders pursued a safe haven flight-to-quality trade. More recently the huge monetary and fiscal stimulus and the prospect of federal budget deficits have been factors causing the dollar to fall. The Federal Reserve’s policy to keep short-term interest rates near zero until 2023 is also pressuring the dollar lower.

RED FLAGS:

The 2020 market produced great returns but trees don’t grow to the sky. There are notable “Red Flags” that warrant scrutiny and consideration.

–Fed Put. The Fed “Put” is seen as a Backstop: the so-called Fed “Put” continues to provide investor support based on the widespread belief that the Federal Reserve will move aggressively to prevent or at least mitigate any deep market swoons. Although there is no actual Fed Put trade, (Put Option trades offset market downside risk), Fed actions are seen as providing “Put-Like” protection against severe market declines. In any event, the Fed Put narrative encourages risk taking without having the actual wherewithal to prevent a severe market decline.

–FOMO: The recent market strength has surprised many institutional investors, and there does appear to be an element of FOMO-the Fear Of Missing Out. Markets trade on fear and greed, and the current market strength appears to have a significant amount of momentum-based trading. The current greed factor can be reversed quickly, as was seen this past March.

–IPOs-Initial Public Offerings: U.S. Initial Public Offerings (including Special Purpose Acquisition Corporations) raised a record $167 billion in the U.S. during 2020, compared with the previous record of $108 billion during the 1999 dot-com boom, according to Dealogic. These deals have jumped roughly 18% on their first day of trading, and there is a concern that the market is getting too frothy.

Margin Debt and Options Contracts-Investors borrowed a record $722 billion in margin debt against their investment portfolios through November according to the Financial Industry Regulatory Authority. High margin debt levels preceded market peaks in 2000 and 2008. Option contract volume has also been at record levels. Call option contracts and other derivative strategies can be very lucrative in bull markets, but can be disastrous in sharp market declines.

New Retail Investors and Robinhood: Market observers point to increased retail investment activity by newer and less experienced investors. The Robinhood trading platform grew rapidly by offering zero commission trades and an appealing user interface. Charles Schwab, Fidelity and others quickly matched Robinhood’s zero commission trades. With big 2020 gains, investing has been eurphoric, just as it was for day traders in 1999. No one knows where markets are headed on a short-term basis, but the Robinhood phenomenon is a clear red flag.

The Red Flags listed above are not a call to sell all and go to cash. Time in the market is more important than timing the market. But the analysis points to a disciplined approach to rebalancing and tactical adjustments away from high-flyers and towards under-owned and cheaper asset classes like small caps and emerging markets. It is also a cautionary warning against the long-maturity bonds.

Wrapping Up:

2020 was a year like no other. The word “Unprecedented” was used often because it is hard to find another word to better describe the year.

To recount a few examples:

-Deaths, ICU units at capacity, temporary hospitals in parking lots.

-Health care and essential workers pushed to the limit.

-Record short vaccine timeline development.

-Charitable giving and acts of compassion.

-Numerous investment and economic records for depths, heights and speed.

Looking to 2021:

Thanks to vaccines we can look forward to a better year as we can re-connect with family, friends and work associates.

The markets are less predictable but we can say a few things:

-Last year’s gains were surprising, and the future will bring more surprises, both good and bad.

-Last year ended up being a good year in the market but it is important to never confuse a bull market with brilliance.

-Markets are noted for teaching great humility and that definitely applies to this analysis. The commentary is intended to provide educational perspective, but only time will tell what the future actually brings.

-No one knows exactly when the music stops, but a proactive, disciplined approach is essential to providing good long-term returns.

Interest Rates at 0.01% at your bank! This dates me but I remember my first mortgage at 9%. At the beginning of 2020 the economy was progressing on cruise control, unemployment was at low levels not seen in 50 years and you could earn roughly 2% on your money market fund. Nobody foresaw the COVID19 pandemic, a million+ lives lost and a global recession. Little did we know that Clorox, Peloton, Netflix and Zoom would be so important in our lives. The financial markets reacted violently with stocks first plunging 35-50% and then recovering at historic speed to all-time high levels. Interest rates reacted as well. Deposits at checking and savings accounts, money market funds and other short-term investments dropped precipitously, often to 0.01%. That’s one penny earned in one year on a $100. Talk about getting rich slowly. On the scale of things, this is not one of the biggest problems, but it is worth considering alternatives.

The Federal Reserve did what it had to do.

The Fed reacted to the COVID-induced shutdown and recession by driving down interest rates to support an economy that was in free fall. The Fed (with lessons learned from the Great Recession of 2008/2009) did a superb job and likely prevented a Depression. By driving down interest rates, they made borrowing much cheaper for car loans, mortgages, educational loans and for corporate borrowers to keep businesses running and people employed. But driving down interest rates also impacted deposits at financial institutions.

Banks, brokerage firms and other financial institutions reacted by reducing rates they paid on deposits to near zero. (It seems like a long time ago, but many money market funds were paying over 2.25% in 2019.) Banks and brokerage firms have been able to maintain sufficient depositary assets while paying little interest because these assets are “sticky”. It is a hassle to switch to alternative accounts that pay higher interest rates, but it may be worth it.

What You Can Do.

These low rates are not going to pop back up quickly again, either. The Fed has communicated a policy to keep short-maturity rates near 0% until 2023, essentially “Lower for Longer”. For perspective, the Fed kept rates near 0% after the Great Recession for 7 years-from late 2008 through late 2015.

With the prospect of essentially 0% for perhaps the next three years, it makes sense to consider alternatives. Although there is no silver bullet, a high-quality, short-term bond fund makes a lot of sense as a substitute for current money market holdings in cases where there is not a need for near-term liquidity.

Short-Term, High-Quality Bond Funds: A good example is the Schwab Short-Term Bond Fund-SWSBX. There are others as well. For example, the Vanguard Short-Term Bond Fund-BSV is another candidate. In addition to purchases in Schwab or Vanguard, these funds can be purchased in many other brokerage accounts like Fidelity or JP Morgan as well.

The Schwab Short-Term Bond-SWSBX is recommended based on my Cornerstone LLC fund rating analysis.

Recommendation Rationale: Higher Performance and Yields than most bank accounts and money market funds: SWSBX is up 4.18% for 2020 through October 23. The fund’s 12 Month Distribution Yield is 1.84% and the current month distribution yield is 1.17%.

Relatively short maturities and less vulnerable to unexpected rising interest rates. The Duration = 2.75 and Effective Maturity = 2.9 years.

Good Overall Ratings: Morningstar Overall Rating = 4 Stars (1 Star is lowest and 5 Stars is highest). Morningstar ranks it as Above-Average Return and Below-Average Risk compared to the comparable benchmark.

Lower Volatility: The NAV value increased every month in 2020, including March when stocks sank over 30%. It should be noted that this fund could have some negative monthly performance, but total return performance over a longer period of time should significantly exceed bank accounts and money market funds.

Future Performance: Fund Distribution rates and investment performance will likely come down over time as older higher-yielding bonds mature, and are replaced by new bonds that have lower yields.

As with all investments, there is a need to continue to monitor this fund and other alternatives and there may be a need to make changes based evolving market conditions.

Intermediate-Term Investment Grade Bonds represent the next step up in the risk/reward tradeoff. An example is the Vanguard Intermediate-Term Bond Index-VBIIX. This fund has a Credit Quality rating of A, a Duration of 6.5 and a Maturity of 7.4 years. This fund has returned 4.5% annualized over the last 5 years, but it represents more risk, and especially during economic recessions. This fund would also be more vulnerable to a sharp, unexpected rise in interest rates.

Other Alternatives Less Appealing:

Certificates of Deposit: Bank and brokerage CDs are mostly locked in at very low interest rates and look less attractive. Some examples are listed below:

Schwab CDs: APY** 1 to 9 Months: 0.1% 10 to 18 Months: 0.15% 1.5 to 2.5 Yrs: 0.2%

Higher Yielding Online CDs-1 Yr* APY-1 Year Ally Bank 0.65% Marcus Bank by Goldman Sachs 0.65% Synchrony Bank 0.60%

Online Savings Accounts: These online savings accounts likely offer interest rates above your local bank, but you will need to set up the online account. Higher Yielding Online Savings Accounts* APY Vio Bank 0.76% Citibank 0.70% Synchrony Bank 0.65%

Top Online Money Market Accounts: Online money market accounts also require setting up an online account. Higher Yielding Online Money Market Accounts* APY First Internet Bank 0.60% Ally Bank 0.50% Synchrony Bank 0.50%.

* Source = BankRate.com as of 10/23/20 **APY is the Annual Percentage Yield.

Note: The data listed above provides an indication of rates for larger, more well-known names, and it doesn’t necessarily reflect the highest rates. Rates often vary depending on the amount deposited and some of the highest APYs may include monthly service fees. Not all rates have identical terms and conditions, and some rates may be introductory promotional rates. ATM access and fees also varies widely. It is important to carefully review the terms and conditions of each offer before making any investment. The financial institutions listed above are not specifically recommended. Data as of 10/23/2020.

In addition to BankRate.com, other online sources include: BestRates.com DepositAccounts.com. (Lending Tree) BestCashCow.com.

See Cornerstone Investments for more information related to investing and financial planning

Jeff Johnson, CFA October 24, 2020

Disclaimer: The information provided above is for informational and educational purposes and it does not constitute personal investment recommendations or investment advice. The investment information presented is generalized and it does not take into consideration the individualized needs, objectives, constraints or unique circumstances of individual investors. Historic market trends, risks, patterns and relationships may not continue into the future and assumptions and predictions may not prove valid. Past performance does not guarantee future performance. Markets are dynamic and subject to change and all investment commentary is subject to change or revision without notice. Cornerstone uses multiple data sources wherever possible to help provide data and information that is comparable across various asset classes and is consistent over the course of time. All data and content is derived from what are considered reliable and credible sources, but Cornerstone does not accept responsibility for any errors. The user accepts all responsibility for actions taken based on information from Cornerstone Investment Associates, LLC.

We all know that 9/11 changed everything, and so does COVID-19. Stay-At-Home orders, social distancing and masks are now familiar parts of our routine. Just as we evolved from 9/11, we will evolve from the novel coronavirus. Nevertheless, “Unprecedented” seems to be the word that best characterizes the first half of 2020. Listed below are relevant factors:

Noteworthy Movers:

Although the broad stock market was down 3.1% for the first six months of 2020, Clorox was one of the top stock performers with a gain of 45%. Few people knew of Zoom at the beginning of the year, but it is up 6X from it’s April 2019 IPO. More obvious first-half winners include Amazon up 49%, NetFlix up 41% and Apple up 25%. On the speculative side, Tesla was up 158%. Airlines were the obvious losers with Delta down 52%

Index Benchmark Performance As Of 6/30/2020:

Major Benchmark Performance:

Last 3

Last 12

1 Mo

Months

YTD

Months

Since:

5/31/20

3/31/20

12/31/19

6/30/19

As Of:

6/30/20

6/30/20

6/30/20

6/30/20

US Large Cap-S&P 500

1.99%

20.54%

-3.08%

7.52%

US Small Cap-Russell 2000

3.53%

25.42%

-12.98%

-6.63%

Foreign Developed-MSCI EAFE

3.40%

14.87%

-11.36%

-5.15%

Foreign Emerging Mkts-MSCI EEM

7.35%

18.09%

-9.77%

-3.38%

US Bonds-Barclays Aggregate

0.63%

2.90%

6.14%

8.74%

Long Treasury-20 Yr+ US Treasury Bonds

0.13%

0.12%

21.62%

25.97%

High Yield-Bloomberg

0.98%

10.18%

-3.80%

0.03%

The Bear Market struck with a vengeance in March after a record long 11-year bull market and a record long 10 ½ year economic expansion:

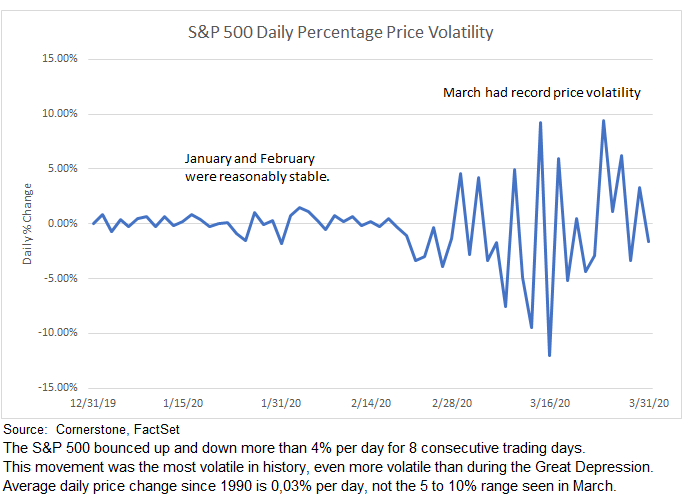

In addition, the drop was accompanied by record-high volatility. The S&P 500 fell from an all-time high to a bear market decline of over -20% in only 22 trading days, the quickest decline in history, even faster than during the Great Depression. Moreover, the S&P 500 set a record of eight consecutive days in which the index moved up or down by at least 4%. Then, the S&P 500 made the quickest recovery in history from a Bear Market to a technical Bull Market (up 20% from a recent low). With the price volatility at record levels in both directions, the overall investment performance has improved significantly since the March 23 lows.

Performance has rebounded since the March lows:

Although the S&P 500 fell -33.9% by March 23 from the all-time high, it is now down only -3.1% YTD as of June 30. The first quarter had the worst performance since the 2008 Great Financial Crisis, and then the second quarter was the best performance since the 4th quarter of 1998. This whiplash was the first time with such extreme quarterly performance since the 1930s. U.S. small caps continue to lag behind the perceived relative safety of larger U.S. companies and are down -13% so far in 2020. Foreign developed equity is down -11.4%. Emerging markets were the big surprise during June with a gain of 7.4%. Longer maturity U.S. Treasury bonds benefited from declining interest rates and from investors seeking a safe haven, and are up 21.6% so far this year. Corporate bonds and especially high yield declined sharply in March due to increasing recessionary fears, but have since recovered somewhat in April through June largely due to the Federal Reserve’s corporate credit support.

Some market prognosticators refer to the big Q2 price recovery as the “Hopium” Trade and the Silly Season, but the reality is that the short-term market is difficult to predict and it forces humility on us all.

Economic Statistics are coming in better than expected:

Although economic statistics initially dropped precipitously due to the government-induced shutdown, they are now showing a significant improvement.

–Unemployment (at a 50-year low of 3.5% in February) spiked to 14.7% in April but has since dropped to 11.1% for June. Although this unemployment level is still a high level, it reflects the addition of 4.8 million new jobs and it was much better than the market expected.

– The Conference Board reported that its Consumer Confidence Index rose to a reading of 98.1 for June from 85.9 in May. Economists polled by Reuters had forecast the index rising to only 91.8 for June.

–Retail sales for April declined 14.7%, the largest decline since 1992 when this data series was initiated. However, May retail sales jumped a record 17.7% on a month-over-month basis, well above the consensus expectation of 7.5%. Retail sales were impacted by pent-up demand and government checks, so it is difficult to know what retail sales level will be reported in the future. It is important to note that the May sales report was still down -6.1% on a year over year basis.

-The Leading Economic Indicators came in at a positive 2.8% after falling -6.1% in April and -7.5% in March. These statistics point to the sudden, large shutdown of the U.S. economy caused by the unprecedented coronavirus pandemic, and then an encouraging uptick.

Progress on Vaccines and Treatments:

Vaccines and treatments hold the promise of allowing the global economy to get back closer to normal, and there are numerous reports showing progress. The U.K. government approved the use of dexamethasone, a steroid that cuts the risk of death for patients on ventilators and for those on oxygen. There is also preliminary evidence supporting Gilead Science’s Remdesivir, an anti-viral treatment, and by vaccines from Moderna, Pfizer and others. Moderna was said to “show promise” in phase-one trials and is progressing to phase-two trials. Dr. Anthony Faucci, Director of the National Institute of Allergy and Infectious Diseases, also expressed optimism regarding a relatively quick approval. However, a 12-18 month timeline still looks more likely. Any COVID-19 vaccine would likely be first used to protect front-line health care workers and elderly who are at most risk to the virus. Over time, a vaccine would achieve “herd immunity”, whereby the antibodies of the majority of individuals built up, either via exposure or vaccination, are sufficient to protect the remaining vulnerable people. In the short-term, however, there is clearly a risk of a “Second Wave.” Broad-based testing needs to be expanded so virus carriers can be identified and isolated.

FOMO-the Fear Of Missing Out:

The recent market strength has surprised many institutional investors, and there does appear to be an element of FOMO-the Fear Of Missing Out. Markets trade on fear and greed, and the current market strength appears to have a significant amount of momentum-based trading. Retail trading is up sharply based on commission-free trades and accounts like Robinhood that are said to be having significant trading volumes based on inexperienced traders.

Virus Resurgence:

As states move to reopen, there has been an unfortunate surge in new coronavirus cases and rising hospitalization rates in states like California, Texas, Florida and Arizona. This has once again overstretched the health care system, and especially ICU units. As a result, a number of states have paused or rolled back their re-openings, especially related to bars and restaurants. There is also the prospect of a mutated version of the virus flaring up in the fall and winter. Consequently, COVID-19 remains a global wildcard.

Market Valuations remain rich:

At this point, markets are ignoring weak 2020 corporate earnings, and are trading on expected 2021 earnings. Nevertheless, various valuation metrics (like Price/Earnings ratios) for 2021 are still elevated. It is important to remember that valuation doesn’t predict short-term performance, but valuation definitely impacts long-term performance potential. In other words, markets could continue to move up on a short-term basis, but the longer-term performance might be a 5-7% average return/year rather than the historic 10%/year long-term U.S. stock return average. See Market Valuation

Election Volatility:

According to recent political polls, Vice President Biden is leading President Trump by a significant margin, and the U.S. Senate might shift to control by the Democrats. In the case where the Democrats win the presidency and control both the House and the Senate, then tax increases are likely. Joe Biden has said he would raise the corporate tax rate from 21% to 28%, rolling back Trump’s 2017 corporate tax reforms. Greater restrictions on corporate share buybacks are also likely. A report from Goldman Sachs estimates that such an outcome would shift 2021 earnings per share for the S&P 500 to $150 from a current estimate of $170. It is probably safe to say that a large earnings decline caused by a corporate tax increase would negatively impact market performance. For individuals, higher capital gains tax rates, the elimination of the qualified dividend tax rate, and/or higher tax rates on top income earners are expected. Without getting too deep into tax policy, there is a strong argument that higher corporate taxes makes our U.S. companies less competitive in international markets. To the extent that U.S. companies are less competitive in the international market place, then they don’t expand U.S. operations and they don’t hire U.S. workers.

Stock Market and Economic Disconnect:

The markets were buoyed in the second quarter by progress in “a flattening of the curve”, the prospect of re-opening the economy, and early reports regarding treatments and vaccines. Moreover, recent economic statistics show a stronger-than-expected rebound from the initial dramatic declines. As a result, the market seems to be anticipating a V-shaped recovery. Although a downdraft to the March lows does not appear likely, there are numerous risks that could cause market weakness.

While recent economic statistics have been stronger than expected, they may reflect more pent-up demand rather than long-term growth. Economic growth over the next year faces significant headwinds and is not likely to quickly recover lost output. The economic recovery still looks like a “Nike Swoosh” or even a U-shaped recovery, not V-shaped, and it looks like there is a disconnect between the recent market rebound and the broader economic landscape. Although the market was up in the second quarter, it still looks vulnerable to additional sell-offs. The current situation seems to be the opposite of what happened in December 2018. At that time, the market sold off hard based on fears of a global economic recession, even though the economic data did not show an imminent recession. In January, 2019, Cornerstone described a Market/Economic Disconnect where economic fundamentals in late 2018 were much stronger than indicated by the sharp market decline. This time, however, the economic fundamentals are very weak, but the market has been ignoring these weak fundamentals as it rebounded significantly in April through June. Only time will tell how the coronavirus recession plays out, but it is helpful to stay grounded in longer-term economic and market fundamentals.

It is helpful to remember that Bear Markets since 1950:

-the average bear market declined -35% and lasted an average of 14 months.

-the average bull market gained 199% and lasted an average of nearly 6 years.

Bear markets are typically much shorter than bull markets, they go down less, and they have always given way to another bull market.

The Federal Reserve has been very proactive:

ensuring funding for banks and companies. The Fed re-established many of the initiatives from the 2008 Great Financial Crisis that have proven positive in the past. A major difference is that the Fed established these support programs so quickly. The Fed cut the Fed Funds rate to near zero in an emergency meeting.

The Fed also provided a “do whatever it takes” stance to support lending for small and large businesses, money market funds, state and local governments, and global central banks for foreign investors seeking the safety of the U.S. dollar.

U.S. Fiscal Legislation:

Congress passed a $2.2 Trillion coronavirus aid package to help stabilize the U.S. economy. Key provisions include support for individuals (the Paycheck Protection Plan and increased unemployment benefits), small businesses, large corporations, public health, and state and local governments. This package is being called a rescue plan, and many politicians say there will need to be another round to provide stimulus. As with the Federal Reserve’s timely actions, the legislation is being implemented far faster than was the case in the 2008/2009 Great Recession.

U.S. Federal Budget Deficit:

Morgan Stanley released an estimate of the U.S. budget deficit of $3.7 Trillion for calendar year 2020, and they see an additional $3T in 2021. This would make the deficit approximately 15-20% of the U.S. GDP. This is larger than the 2008/2009 Great Recession level. This analysis does not incorporate the proposed $2T infrastructure bill. Although there is a clear need for monetary and fiscal spending during this downturn, there is also a looming longer-term issue related to U.S. budget deficits.

International:

China was the first country to lockdown its economy in January, and official data show positive economic manufacturing and non-manufacturing growth resuming in March. These reports do not indicate an imminent global turnaround, but they do represent a measure of improvement in China. The Eurozone is experiencing economic improvement from the lows of March and April, but they are mired in an economic recession. Japan is also stuck in a deep recession.

On a global basis, a June International Monetary Fund forecast shows a -4.9% 2020 global economic decline and then a 5.4% recovery for 2021.

What’s Next?

There is no good historic precedent for the coronavirus given that globalization has allowed pandemics to spread much more quickly than in the past. Consequently, we are in the midst of a global recession. The first quarter market downdraft caused a lot of economic weakness to be priced in, but the strong second quarter market performance has now priced in a fairly optimistic outlook. Since the depth and duration of the coronavirus remain unknown, continued market volatility can be expected. With all these crosscurrents, it remains critically important to stay focused on longer-term fundamentals that should gradually improve.

WHAT YOU SHOULD DO:

Portfolio actions that you take (or don’t take) at this point can feel highly uncomfortable but the decisions are not rocket science. Investors were bailing on investment holdings at a near-record pace and then have been charging back in. This is no time to be part of the herd’s stampede in either direction. Although there is much we don’t know about the ultimate coronavirus impact, there is also much we do know. There is nothing unique about the list below, but it is supported by ample historical evidence.

-Stay the course. Fear and Greed are really the biggest risks.

-Don’t sell unless you have a dire need for cash.

-Rebalance the portfolio to restore beaten-down equity holdings to a weight consistent with your long-term investment objectives.

-If you have cash, then add to equity holdings on a systematic basis. This isn’t easy, but a good strategy is to make several smaller investments over time rather than one larger trade. No plan is fail-safe, but this strategy is a way to get into the market without making one big move.

– Remember that investment performance is improved by buying in bear markets, not selling.

-Dollar Cost Averaging that invests a predetermined amount of dollars on systematic predetermined dates is a method that remains a valid investment strategy.

If you think this market is crazy volatile, then you are right. The market fell into a bear market (down -20%) faster than at any time in history, even including the Great Depression. The daily price moves looked more like an out-of-control roller coaster than a rational, orderly market.

Considering this manic behavior, you have to wonder where are the grown-ups? You also have to ask why investment people making the big bucks can change their minds so quickly and erratically. Where’s the conviction? Disciplined or fickle?

The COVID-19 pandemic has been called a Black Swan-a hard to predict rare event that comes as a complete surprise and has a major effect. It has been characterized as a Known Unknown, and it has been a trigger for the market volatility and downdraft. There have been a number of other factors that combined, however, to cause a “Perfect Storm” of Volatility.

Despite the historically high volatility level, there has not been historically bad investment performance. So far, investment performance has been similar to a typical bear market. It is understood, that investment performance could still get worse.

The graph below shows the incredible volatility starting in March.

Listed below is the actual S&P 500 index performance. It is down so much because there were more large volatile down days than up days.

VOLATILITY CULPRITS:

Two key contributors to this Perfect Storm of volatility include:

-Human nature, with all the emotional euphoria on the way up and despair on the way down.

-Big, fast computers. Algorithmic Trading, High Frequency Trading, and increasing use of momentum and volatility strategies represent the second major contributor to the volatility. This trading was magnified by excessive financial (debt) leverage.

(Details are listed further below:)

WHAT DOES IT MEAN FOR YOU?

First, it is important to keep perspective. The main priority is saving lives. Everything else comes back.

It shouldn’t impact your Investment Objectives: It is important to maintain a long-term perspective. The huge volatility in March shouldn’t impact a long-term focus. This is not a financial crisis, but rather a crisis of confidence. The depth and duration of the coronavirus are not known, but it does not appear to constitute the fundamental, systemic problems associated with the 2008 Great Financial Crisis. Moreover, the massive government monetary and fiscal support being implemented is much larger and coming much quicker than in 2008.

The sudden -20% market decline has been painful (especially after 11 big years), but the decline is well within the historic range for bear markets. The market decline should also be remembered within the context of the 31.5% gain by the S&P) 500 in 2019. More importantly, the market will come back.

A review of Bull and Bear markets since 1950 shows:

-the average bear market declined -35% and lasted an average of 14 months.

-the average bull market gained 199% and lasted an average of nearly 6 years.

Bear markets are typically much shorter than bull markets, they go down less, and they have always given way to another bull market.

It might sound flippant, but in a way the market had gone too far too fast and was due for some downside.

It is important to remember that there are wide ranges around the average length and return of bull and bear markets. Nevertheless, history shows that all bear markets end.

Portfolio actions that you take (or don’t take) at this point can feel highly uncomfortable but the decisions are not rocket science. Investors have been bailing on investment holdings at a near-record pace and this is no time to be part of the herd’s stampede. There is nothing unique about the list below, but it is supported by ample historical evidence.

-Stay the course. Fear is really the biggest risk.

-Don’t sell unless you have a dire need for cash.

-Rebalance the portfolio to restore beaten-down equity holdings to a weight consistent with your long-term investment objectives.

-If you have cash, then add to equity holdings. This isn’t easy, but a good strategy is to make several smaller investments over time rather than one larger trade.

– At this stage in the bear, there is likely to be far more upside than downside. Remember that investment performance is improved by buying in bear markets, not selling.

It’s Deeper than Fear and Greed — Non-Investment Observations:

It is often said that the markets run on the animal spirits of Fear and Greed. It’s not really that simple. It’s too early to know the depth and duration, but here are some non-investment observations:

-It would be a mistake to bet against the resilience, creativity and persistence of Americans in this time of challenge.

-Health care workers are showing incredible dedicated service despite personal risk and sacrifice and are a true inspiration. This is especially true for the nurses who have the most frontline exposure.

-Essential workers are taking on a new meaning as we see who really is essential.

-Human ingenuity from both the government and the private sector are working furiously and there are good reasons to remain optimistic.

-Many companies are forgoing profits and are keeping employees or paying what they can.

-The general public is showing impressive broad-based acceptance and support for social distancing and quarantines. It has changed lives, but everyone seems to recognize that we are all in this together.

-There are uncounted and often un-noticed acts of helping and compassion that add up to something much bigger.

When considering all this, I am reminded of Genesis 1:27 where it says that we are created in the image of God. It is gratifying to see humanity set aside mundane differences and rise up to face this challenge. These are the times that bring out the best in all of us.

DIGGING DEEPER-VOLATILITY DRIVERS

Human Nature-Complacency and then Panic:

Investors received stellar performance during the longest bull market in history, 11 years, and this was accompanied by the longest economic expansion in history, a stretch that ran for 10.5 years. For years, investment performance ratcheted upward, causing a sense of complacency. Central banks around the globe kept interest rates low, and encouraged investments in riskier assets. Investing was characterized by the Fear Of Missing Out-FOMO. With this benign backdrop it is little wonder that the sudden recognition of the coronavirus was a major factor that upset the apple cart and caused such volatile emotional selling.

Economic prospects-V-Shaped Recovery, or U, or L: Epidemics historically cost lives but have not had big longer-term impacts on markets or the economy. This time it looks different. The speed and suddenness of the global shutdown is unprecedented and economists and others are only gradually beginning to understand the magnitude of this change and then to incorporate this into their models. For example, Goldman Sach’s initial analysis of COVID-19 impact foresaw minimal impact to the U.S. and they saw 1.2% US GDP growth for 2020. A subsequent forecast revised U.S. 2020 economic growth to 0.4%. As of March 21, Goldman has significantly revised their 2020 GDP growth rate down to -3.8%. This forecast includes a -24% annualized negative growth rate for Q2 and then a sharp Q3 recovery of 12% annualized and Q4 gain of 10%. This analysis sees a V-shaped recovery.

The point is not to throw rocks at Goldman Sachs, because they are smart, savvy investors. The point is that analysts are increasingly negative about near-term prospects. Further, it warrants caution regarding how much we really comprehend about the coronavirus impacts. Given the unprecedented nature of the shutdown, it seems that there may be more caution by both consumers and companies as we emerge on the other side and a U-shaped recovery is more likely than a V. Finally, the coronavirus outbreak may prove to be worse than the 9/11 terrorist attacks, but it doesn’t look to be as severe as the full-blown 2008/2009 Great Financial Crisis.

COVID-19 Backdrop: As 2020 began, investors were optimistic the economic expansion would continue, as calming trade tensions between the U.S. and China and three 2019 interest-rate cuts from the Federal Reserve lifted stocks. The coronavirus was widely publicized by mid-January, but it was first ignored and markets went on to post all-time record highs by February 19. For years, it paid to buy each dip in stocks and to embrace trades that bet against the return of volatility. Then the COVID-19 virus became increasingly problematic and ultimately caused an unprecedented global shutdown. Millions of the nation’s businesses suddenly closed their doors, international travel ground to a sudden halt, and personal interactions were sharply curtailed. Markets reacted negatively with unprecedented volatility. As the severity of the situation became increasingly apparent, economic and earnings forecasts were repeatedly revised down lower and lower. The transition from complacency to a sudden, unprecedented global shutdown caused a huge emotional reaction and produced panicked selling.

ALGORITHMIC TRADING:

Algorithmic trading was the other major factor in the huge March volatility. Algorithmic trading essentially involves computer programs that follow defined sets of instructions (algorithms) to do stock trading far faster than humans can do. It often utilizes back-testing of technical indicators like movements of 50-day and 200-day moving averages, trend following patterns and arbitrage opportunities based on pricing anomalies.

Algorithmic trading is different from fundamentally driven trading that is based on rigorous analysis of company valuation and revenue and earnings growth prospects. Instead, “algo” trading looks for relatively small market dislocations and inefficiencies that can be rapidly exploited with strategies related to volatility, momentum and risk parity. Quite simply, it’s not based on strong company earnings growth or an attractive valuation level. Analysts at J.P. Morgan said “fundamental discretionary traders” accounted for only 10% of recent stock trading volume. Goldman Sachs analysis shows equity algorithmic trading is nearly 3 times the level from 15 years ago.

High Frequency Trading-HFT: Algorithmic trading is often based on High Frequency Trading (HFT) that utilizes powerful computers moving in and out of markets at lightning speeds measured in milliseconds. In normal markets HFT adds liquidity and lowers costs by reducing bid-ask spreads on trades. In March, however, profits at the large HFT algorithmic traders were reported to be extremely high, and there is now a question about the value of HFT in times of market duress.

Volatility Trades: The 11-year bull market was accompanied by a below-average level of price volatility. In this environment, hedge funds and other institutional investors utilized a variety of algorithmic strategies to trade on small changes in market volatility, regardless of whether they went up or down. Since price volatility was low, many of these strategies used financial leverage at up to 10X. As markets moved up, low volatility caused traders to buy risky assets. As markets fell, volatility rose and the computers began selling. As a result, during March this computer-based trading magnified both moves upward and downward. In another example, investment strategies were established by market participants to either dampen volatility or enhance returns based on previously reliable relationships between assets. Unfortunately, these pricing relationships fell apart when volatility spiked and caused devastating effects in panicked markets.

Six Sigma: The Wall Street Journal reported prices gyrating by an incredible six standard deviations from the short-term norm. These moves were exacerbated by the presumed low likelihood of extreme market moves with risk models largely based on a period of relative market calm. Since many of these trading strategies were structured with high financial leverage, it became a situation where everyone headed for the exit at the same time. It is easy to see how unwinding these trades caused such panicked selling.

Momentum Trades also benefit from Algorithms: Momentum trading is an investment strategy that has a good historic track record. Momentum traders buy the stocks that are going up the fastest. Or they might buy the stocks that have the greatest revenue or earnings momentum. Regardless, this feeds on itself and the more momentum traders, the more it spirals upward. When markets (or stocks) reverse and head down, then momentum traders are selling the assets that are falling the fastest. They essentially turbocharge the upward buying interest and then magnify the downward selling pressure.

Fundamentals prevail over Algos on a long-term basis: Since Algorithmic trading is focused on short-term factors like volatility and momentum, it has less relevance to fundamental factors. Fundamentals still function to differentiate the merits between various companies and future prospects, and fundamentals still determine the long-term performance of investment assets. What this means to a long-term investor is that algorithms probably reduce trading costs by a small amount during normal market activity, but a disciplined investment process still prevails on a long-term basis.

Liquidity Dried Up:

Liquidity in the financial markets means the ability to sell an investment asset quickly without having to sell it at a big discount. Liquid investment assets usually have a large number of buyers and sellers readily available so that a transaction is easily traded and it minimally impacts the price. US Treasury securities normally have the greatest liquidity. Your house is far less liquid. The sudden shutdown of the U.S. economy was unprecedented and it precipitated an immediate dash for cash.

Dash for Cash: Individuals suddenly faced unemployment or reduced hours, particularly in the airline and entertainment industries. Businesses, seeing markets and revenue shutting down, drew down bank credit lines. Small business owners were particularly vulnerable because they typically lack the financial flexibility of larger firms. Fund managers faced redemptions as investors liquidated holdings. Traders attempted to unwind trades that had worked in a low volatility investment environment. In many of these cases, normal cash flow patterns were disrupted and caused an immediate need for cash.

US Treasuries & Gold-Traditional Safe Havens Didn’t Work:

US Treasuries prices typically rise (and yields drop) when investors seek a safe haven. This time, Treasurys dropped the at the same time stock prices were dropping, so there was no safety anywhere.

The Treasury market was disrupted by other factors as well. For example, even short maturity Treasury securities (due in 30 days or less), sold off because people wanted cash, NOW!

Gold is another asset the investors buy in scary times, but gold actually declined at the same time that the stock market began falling.

Risky Assets were Crushed:

With fears of an imminent recession, investors fled riskier debt, afraid companies that loaded up on credit amid low interest rates would have trouble repaying. These assets became extremely illiquid, and the only way to unload them was to sell at a huge discount. As an example, the high yield (junk bond) Exchange Traded Fund- HYG quickly fell 15%. Somewhat ironically, investment managers during times like this are typically forced to sell their highest-quality assets because the discounts on lower quality assets are so extreme.

Short Covering:

Short covering is often the cause of markets spiking upwards. A short trader essentially uses a derivative security to sell an investment asset today with the provision to buy it later before a specified date. For example, a short trader hopes to sell a stock today for $100, and buy it in the future at $90, a lower price. This can be extremely risky, but it can be lucrative. When the market is going up instead of down, this trade becomes increasingly unprofitable. You have already sold at $100, and now you have to buy at perhaps $110 or more. As the market goes up, short traders have to sell (Cover) before they lose even more money. A large number of short sellers covering (closing out their increasingly unprofitable trade), means prices go up even higher. This was a part of the reason that the S&P 500 went up 9.4% on March 24. Many times, large upward price moves are caused by short covering.

Margin Calls:

Investors are allowed to borrow money in their brokerage accounts to buy even more stock. This works great in rising markets, and it made you feel like a rock star in 2019 when the S&P 500 went up 31.5%.

When stocks decline, investors are required to put in more collateral. They need to add to their margin account. When they don’t have the cash, their broker will liquidate some of their securities to re-establish their required margin. This is a “Margin call”. Obviously, the more selling pressure in the market place, the greater the number of margin calls and this results in a negative downward spiral. Margin calls were a major negative factor in the 1929 stock market crash.

Final Comments:

These Cornerstone blog posts are designed to provide education and a long-term perspective related to investments. The commentary relies on my career experience, credible sources and hard data as much as possible. Even so, there are always many surprises and unexpected outcomes and this certainly applies to the comments listed above. As always, your feedback is helpful and beneficial.

The longest bull market in history, 11 years, ended March 12, 2020.

The longest economic expansion in history, 10 and a half years, is likely to end.

The fastest move in history for the S&P 500 index from an all-time record high to a Correction (down more than 10%) in six trading days and a Bear Market (down more than 20%) in 16 trading days.

Biggest down day since 1987 with the S&P 500 down 9.5% on March 12.

Biggest up day since 2008. A day after the ominous sell-off, the S&P 500 rebounded 9.3% on March 13.

The CBOE Volatility Index, a closely watched measure that is often called the “Fear Gauge”, rose to its highest level since 2008.

The Stoxx Europe 600 index shed 11.5% on March 12, its worst one-day performance on record. It is down 32.0% from its recent peak.

What’s Next?

No Good Precedent: There is no good historic precedent for the coronavirus given that globalization has allowed pandemics to spread much more quickly than in the past. As a result, a recession, both globally and in the U.S., looks likely.

Although a recession looks likely, the current market downdraft means a lot of economic weakness is already priced in. Nevertheless, the depth and duration of the coronavirus remain unknown and continued volatile market downdrafts can be expected.

Different than 1987: The coronavirus outbreak does not look like the 1987 market crash. Earlier in 1987 both the Dow Jones Industrial Average and the S&P 500 set all-time high records. Then by October 19, 1987, the Dow plunged 22.6% and the S&P 500 dropped 20.5%. Although economists forecast a recession at that time, the economy continued to grow and did not experience a downturn. This time, the coronavirus disruption looks likely to induce an economic recession.

9/11 Surprise: The terrorist attacks in September 2001 caught everyone by surprise. At the beginning of 2020, most investors expected continued market gains for 2020, but the coronavirus has caused another surprise. There was a mild recession associated with 9/11, but markets had already sold off hard for 18 months due to the internet/tech crash. At this time, there are too many unknowns associated with the coronavirus to assume a mild recession.

Different than 2008: The coronavirus outbreak is much different than the 2008 financial crisis and Great Recession. That downturn was driven by fundamental, systemic weaknesses that needed time to correct. The good news is that the Federal Reserve learned a lot during the 2008 crash, and they are able to apply the lessons learned to the current situation.

Liquidity: The U.S. government has stepped in aggressively to provide much needed liquidity. This is critically important for the airlines, energy companies, entertainment companies, restaurants and other small business operators who are facing short-term disruptions caused by the sudden social distancing and retrenchment in normal consumer behavior. The banks who lend to these companies are not structured to provide funds so quickly. Banks typically hold short-term U.S. Treasury securities that mature (become liquid) in weeks or months. In cases where companies suddenly need to borrow funds quickly, the banks lack ready cash. However, the banks can turn to the government to secure these “liquid” funds immediately and then lend these funds to these troubled companies. Keeping these companies afloat is important to maintaining employment.

Liquidity is also being provided to a wide range of institutional investors who are involved in a wide range of lending and foreign currency transactions.

President Trump has declared a national emergency and the U.S. government is providing broad-based support:

-to free up billions in assistance to states and provide authority as the rapidly spreading virus upends life across the country. This would also open up access to up to $50 billion in financial assistance for states, localities and territories.

-to call on every U.S. state to immediately set up emergency operations centers and every hospital in the country to activate emergency preparedness plans.

When these measures were announced on March 13, equity markets shot upward quickly.

Congress last week passed an $8.3 billion measure to help the government develop a vaccine and provide money for states to expand their lab-testing capacity and attempt to limit the damage from the virus.

-Legislation is being structured that would make coronavirus testing free and provide paid sick leave to many of those affected by the pandemic.