The longest bull market in history, 11 years, ended March 12, 2020.

The longest economic expansion in history, 10 and a half years, is likely to end.

The fastest move in history for the S&P 500 index from an all-time record high to a Correction (down more than 10%) in six trading days and a Bear Market (down more than 20%) in 16 trading days.

Biggest down day since 1987 with the S&P 500 down 9.5% on March 12.

Biggest up day since 2008. A day after the ominous sell-off, the S&P 500 rebounded 9.3% on March 13.

The CBOE Volatility Index, a closely watched measure that is often called the “Fear Gauge”, rose to its highest level since 2008.

The Stoxx Europe 600 index shed 11.5% on March 12, its worst one-day performance on record. It is down 32.0% from its recent peak.

What’s Next?

No Good Precedent: There is no good historic precedent for the coronavirus given that globalization has allowed pandemics to spread much more quickly than in the past. As a result, a recession, both globally and in the U.S., looks likely.

Although a recession looks likely, the current market downdraft means a lot of economic weakness is already priced in. Nevertheless, the depth and duration of the coronavirus remain unknown and continued volatile market downdrafts can be expected.

Different than 1987: The coronavirus outbreak does not look like the 1987 market crash. Earlier in 1987 both the Dow Jones Industrial Average and the S&P 500 set all-time high records. Then by October 19, 1987, the Dow plunged 22.6% and the S&P 500 dropped 20.5%. Although economists forecast a recession at that time, the economy continued to grow and did not experience a downturn. This time, the coronavirus disruption looks likely to induce an economic recession.

9/11 Surprise: The terrorist attacks in September 2001 caught everyone by surprise. At the beginning of 2020, most investors expected continued market gains for 2020, but the coronavirus has caused another surprise. There was a mild recession associated with 9/11, but markets had already sold off hard for 18 months due to the internet/tech crash. At this time, there are too many unknowns associated with the coronavirus to assume a mild recession.

Different than 2008: The coronavirus outbreak is much different than the 2008 financial crisis and Great Recession. That downturn was driven by fundamental, systemic weaknesses that needed time to correct. The good news is that the Federal Reserve learned a lot during the 2008 crash, and they are able to apply the lessons learned to the current situation.

Liquidity: The U.S. government has stepped in aggressively to provide much needed liquidity. This is critically important for the airlines, energy companies, entertainment companies, restaurants and other small business operators who are facing short-term disruptions caused by the sudden social distancing and retrenchment in normal consumer behavior. The banks who lend to these companies are not structured to provide funds so quickly. Banks typically hold short-term U.S. Treasury securities that mature (become liquid) in weeks or months. In cases where companies suddenly need to borrow funds quickly, the banks lack ready cash. However, the banks can turn to the government to secure these “liquid” funds immediately and then lend these funds to these troubled companies. Keeping these companies afloat is important to maintaining employment.

Liquidity is also being provided to a wide range of institutional investors who are involved in a wide range of lending and foreign currency transactions.

President Trump has declared a national emergency and the U.S. government is providing broad-based support:

-to free up billions in assistance to states and provide authority as the rapidly spreading virus upends life across the country. This would also open up access to up to $50 billion in financial assistance for states, localities and territories.

-to call on every U.S. state to immediately set up emergency operations centers and every hospital in the country to activate emergency preparedness plans.

When these measures were announced on March 13, equity markets shot upward quickly.

Congress last week passed an $8.3 billion measure to help the government develop a vaccine and provide money for states to expand their lab-testing capacity and attempt to limit the damage from the virus.

-Legislation is being structured that would make coronavirus testing free and provide paid sick leave to many of those affected by the pandemic.

-Proposals are being discussed to help laid off workers, including direct cash payments that are along the lines of the 2008 policy response.

-Initiatives are in process to establish low-interest loans for small businesses.

-Consideration is being given to student debt relief.

Foreign Government actions are being crafted across the globe to provide similar monetary and fiscal stimulus packages.

There is an open question about whether these initiatives will be sufficient, or whether they are already too far behind the curve. There are also some that say these actions are over-reacting. Given the unprecedented nature of this pandemic, it seems prudent to respond as aggressively as possible.

For More Details See Below:

The Coronavirus was largely unknown in mid January, but it has since morphed into a global phenomenon. As of March 10, the World Health Organization reported 113,702 confirmed cases and 4,012 deaths. China is the epicenter of the outbreak, but South Korea, Iran and Italy are also hard hit. The U.S. has 1,267 cases and 38 deaths as of March 11, 2020. Harvard epidemiologist Marc Lipsitch has estimated that between 20% to 60% of adults world-wide might catch the disease. Although the coronavirus has spread across the globe, the newly reported cases in China are declining and Chinese workers are beginning to go back to their jobs. In addition, Reuters is reporting that new cases in South Korea are falling behind the number of patients who recovered and this could be an indication that the outbreak is slowing. There are also reports that the coronavirus is more lethal for smokers and for people living in areas of poor air quality. If this is the case, then some early cases may have overstated the risk to a broader population that has fewer smokers and better air quality.

Due to a lack of testing in the U.S., we don’t know how many Americans are infected. Although social distancing is helping reduce the spread, it is possible that the number of people already infected is far greater than currently reported cases suggest. If the number of cases exceeds current expectations, then hospitals might experience a surge in patients and the healthcare system might become overwhelmed.

Panicked Selling: While the coronavirus has been a human tragedy, it has also negatively impacted global markets with waves of panicked selling based on the fear of the economic fallout on a global basis. For example, the S&P 500 index fell 9.5% on March 12, the greatest one-day decline since October 1987. Then the index rebounded 9.3% on March 13.

Ironically, equity markets first ignored the early reports of the coronavirus in January. During February, new records were set for the S&P 500, Nasdaq, the Dow Jones Industrial Average, and the European Stoxx 600. In fact, he S&P 500 set an all-time record high of 3,386 as recently as February 19, just before plummeting 13.0% in the next seven trading sessions. As an indication of the panic, The Wall Street Journal reported that this was the fastest decline on record from a record high to a correction of below -10% and also the fastest bear market sell-off below -20%. This selling pressure has been exacerbated by President Trump’s 30-day travel ban on persons coming from Europe and continuing cancellations or suspensions of large conferences and entertainment events. The S&P 500 index is now down 19.9% from the February 19th all-time high, and down 15.8% on a year-to-day basis. Small cap stocks have been hit even harder based on the fact that they have less overall financial strength than larger, more established companies. International stocks are down even more than U.S. stocks. Meanwhile, so-called safe-haven U.S. Treasury bonds are up 13 percent year-to-date and an incredible 31% over the last year. These bonds have performed well because the bond prices have moved up sharply as interest rates declined.

Past Epidemics were historically short-lived: Although it is difficult determine the global impact, the Severe Acute Respiratory Syndrome-SARS epidemic in 2003 reduced Chinese GDP by an estimated -0.8%. Analysis by Charles Schwab found that for the 13 global epidemic outbreaks since 1981, the MSCI World Index gained 0.8% in the month after the outbreak, and 7.1% after six months. Morningstar examined the companies that they followed after the SARS outbreak and found no significant long-term effect. In addition to SARS, other notable outbreaks that did not have a significant global impact include the avian flu in 2006, swine flu in 2009, Ebola in 2014, and Zika in 2016. The coronavirus was categorized a pandemic on March 11th, however, and it looks like it will have a much more negative impact than past outbreaks.

History indicates that the market overreacts to short-term headlines and these previous outbreaks did not have a negative impact on longer-term performance. Nevertheless, the current coronavirus appears to have a much bigger impact because China now represents a much larger share of the global economy. Data from the World Bank shows that China’s GDP was at $1.3 Trillion in 2003 during the SARS outbreak and now GDP is $13.6 Trillion. In addition, global exports grew from $438 billion in 2003 to $2.5 Trillion in 2018. Finally, visitors from China to the U.S. grew from 157,000 in 2003 to 2.8 million in 2018. Consequently, there is much greater downside potential than in the past.

Global Economy: Although the Chinese economy appeared to be improving by the end of 2019, the coronavirus is clearly causing a downdraft. The Chinese National Bureau of Statistics reported that the official February manufacturing survey declined from a stable level of 50.0 in January to 35.7 in February, the lowest manufacturing level ever recorded. In addition, the official services data showed a decline from 54.1 in January to 29.6 in February. Although there are reports of Chinese workers beginning to go back to work and some recovery is expected, it is clear that Chinese economic growth will be significantly impacted. The Euro area and the UK were also experiencing improving economic prospects at the beginning of 2020. Germany and Japan were the two major countries with weak year-end economic performance.

The U.S. is described as starting from a good place with solid economic fundamentals. For example, The Citi Economic Surprise Index showed a solid 69.6 rating at the end of February. In addition, the March 6th employment report showed employment gains of 273,000, well above estimates. Although this report covered a period before the coronavirus was seen as a problem, it does indicate the economic strength and momentum going into the coronavirus headwind.

Oil Price War: Russia did not agree to crude oil production cuts proposed by OPEC to support crude oil prices as oil demand fell due to the coronavirus impact, so Saudi Arabia countered with crude oil production increases. These actions essentially resulted in an oil price war between Saudi Arabia and Russia. This pushed crude prices down to $30 per barrel and it contributed to the massive March 9 stock market decline. For the U.S., lower oil prices are a clear benefit for consumers. However, lower oil prices hurt the oil exploration and production segment of the oil industry. Many of these companies have their production hedged (to lock in their prices), but these hedges will roll off going into 2021. If oil prices do not improve over the intermediate term, then many companies will face defaults and even bankruptcy. On an overall basis, there is significant economic analysis showing the benefit of lower oil prices to consumers is roughly offset by the losses to the exploration and production companies. Consequently, falling oil prices may impact short-term U.S. market volatility, but the net longer-term impact to the U.S. economy should not be large.

Deteriorating credit conditions are the clear issue. High yield funds that hold non-investment grade “junk” bonds will experience increasing defaults and bankruptcies, and this will lead to weaker investment performance.

Forecasts: The term Unknown Unknowns might seem appropriate to describe the current environment because it is difficult to know the depth and duration of the spread of the coronavirus. It now seems clear that previous analysis and forecasts from Goldman Sachs, Deutsche Bank and others were too optimistic, as they projected a direct short-term impact on Chinese GDP but minimal impact to the global economy. Recent forecasts are now recognizing a greater negative impact. For example, the Organization for Economic Cooperation and Development-OECD reduced their 2020 global growth forecast from 2.9% to 2.4%. Given the fact that the coronavirus is still spreading and there is no way to know when it peaks, it seems likely that global growth will be reduced by at least 0.5% and the global economy may even dip into recession.

The Wall Street Journal consensus forecast (conducted March 6-10) shows a 49% chance of a U.S. recession in the next twelve months compared to a 26% chance a month ago. On an annual basis, the WSJ survey shows U.S. GDP down -0.1% in Q2, and up 1.2% for the full year. Based on recent data and analysis, it appears that the short-term economic downdraft may be deeper, but prospects for 2021 should be much less impacted. Initially, many economists saw a V-shaped recovery, with a negative impact in the first quarter and then a second quarter recovery. More recently, there is more commentary about a U-shaped recovery. A prolonged L-shaped economic period is also possible if the coronavirus proves worse than expected. It needs to be said that forecasts often initially understate the magnitude of significant declines. For example, practically no one foresaw the depth or duration of the Great Recession. The reality is that there is also an epidemiology factor that is new to economists’ models. Only time will tell, but a global recession appears likely.

Interest Rates: One notable aspect of the current market decline has been the precipitous decline in interest rates. The 10-year U.S. Treasury bond interest rate declined to a record-low level of 0.5% on March 9. Part of this decline is due to concerns of weaker economic growth, but a flight to quality is a greater factor. When market participants grow fearful, they seek safe havens by buying U.S. Treasury bonds. These panicked purchases drove the price of the bond up and the yield down and caused long U.S. Treasury bonds to gain over 30% in the last year. As fears eventually subside, the price will go down and the yield will rise, setting the stage for huge Treasury bond losses.

Federal Reserve: In reaction to the coronavirus economic threat, the U.S. Federal Reserve executed an emergency half-percentage point rate cut to a range of 1.0% to 1.25%, down from the previous range of 1.5-1.75%. The Fed is also likely to reduce interest rates even further at the upcoming FOMC meeting on March 17th and 18th. The difficulty is that the Fed is best positioned to deal with weak aggregate demand, and the coronavirus represents a supply-side shock related to disrupted supply chains. Lower interest rates would help keep the U.S. dollar lower (to help maintain U.S. exports), but lower interest rates don’t create what is really needed-a vaccine. If economic prospects weaken, however, then Fed-induced interest rate cuts will help support aggregate demand. The Federal Reserve has also been an active buyer of short-term Treasury securities to maintain liquidity and an orderly market.

Fiscal Policy: Countries around the world are playing catch-up to the fast-paced coronavirus developments. President Trump has signed an $8.3 billion emergency spending bill. There is also discussion related to payroll tax reductions and low-interest small business loans, but political realities may hamper any significant bipartisan legislation. Globally, there are numerous fiscal policy initiatives that may prove beneficial. Since interest rates in the developed world outside the U.S. are extraordinarily low or negative, there is less potential monetary support. From an economic perspective, tax cuts have the greatest multiplier effect.

It’s not 2008: While the market sell-off has been reported as the worst decline since October 2008, it should not be compared to the 2008 global market meltdown and Great Recession. Back then, there were significant fundamental issues related to over-valued real estate, highly speculative financial transactions and insufficient capital for the global banking system. We don’t know when the number of global coronavirus cases will begin to decline, but it does not appear to be on a scale similar to the massive systemic breakdown from the past.

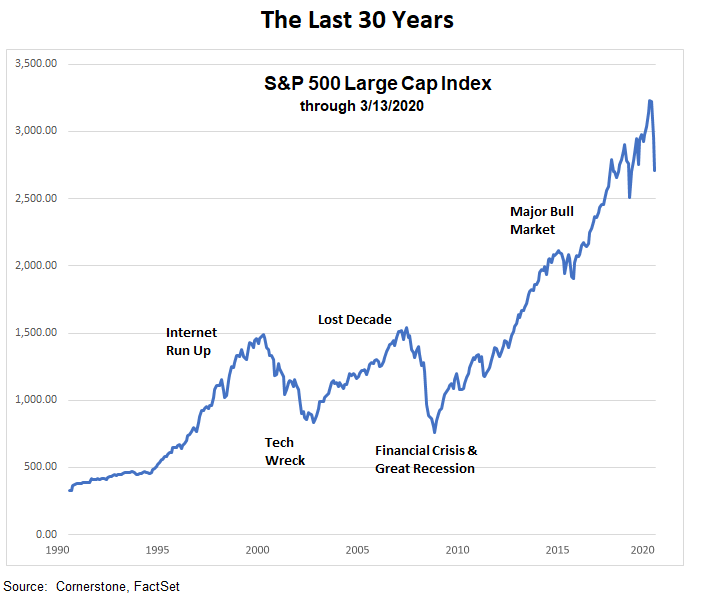

A Good 30 Years: The quick 2020 sell-off erased significant portfolio value through mid March, and it could get worse before it gets better. That being said, it is helpful to remember that the S&P 500 gained 31.5% in 2019. In addition, it is up 422% on a total return basis (and up 14.0% annualized) as we pass the 11th anniversary of the bull market that started March 9, 2009. Market complacency had become pervasive over the past 11 years. The U.S. has been in the longest economic expansion on record, and the S&P 500 has been in the longest bull market without a -20% bear market. It is important to remember that historically going back to 1950, market corrections (down more than -10% from a recent high) occur once every 2.5 years and bear markets (down more than -20%) occur every 7.8 years. Based on these averages, it puts the current decline in perspective.

Additional Thoughts: Although there has been panicked selling, there is also cash on the sidelines waiting to get into the market and these two factors can cause increased price volatility. Moreover, the market is forward-looking and is attempting to front-run “Peak Virus.” In other words, when new cases and deaths begin to diminish, then this will indicate less economic downside and better corporate earnings. However, there is likely to be a series of negative news reports about downgraded economic forecasts and corporate earnings reductions. This will likely include the prospect of a global recession and a recession in the U.S. These negative reports will provide continuing market angst and downside market volatility. Given that the depth and duration is not known, this peak virus event might be in a month but it will probably be much further out. On the plus side, the sell-off has driven market valuation levels much lower and recessionary risks are already partially priced in. For investors with cash, now is the time to begin buying equities. Rather than trying to nail the bottom, it can be advantageous to average in with several investment moves over the course of time.

WHAT YOU SHOULD DO: Although there is much we don’t know about the ultimate coronavirus impact, there is also much we do know:

-First, remember that emotional reactions to short-term headlines are the biggest risk. As hard as it is, investors should not abandon long-term investment objectives.

-Use the current market volatility to rebalance portfolios back into alignment with your long-term investment objectives and asset allocation plan.

-If you have cash to be invested, then this sell-off looks like a good time to invest potentially one third of your idle funds. Then set a date in three months to invest another third or if the market drops another 10%. Finally, set a date in six months to invest the last third or sooner if the market drops by 20%. If the market declines further, you will be getting in at lower prices. If the market moves upward, your first purchases will be at lower prices. No plan is fail-safe, but this strategy is a way to get into the market without making one big move.

Jeff Johnson, CFA

March 14,2020