While “unprecedented” was the word to describe COVID- plagued 2020, the year 2021 had its own share of unique developments, surprises and disruptions.

Bitcoin and other cryptocurrency names gained more mainstream acceptance from both retail and institutional investors despite record volatility.

Meme stocks became the rage as GameStop started the year by jumping over 2400% by late January as retail investors waged a David vs Goliath battle with hedge funds and other institutional investors.

Inflation: As the year progressed, inflation escalated to levels not seen in nearly 40 years.

Everything Rally– Investor IRA, 401k and taxable accounts advanced nicely as markets provided a third year of big gains.

Wild West in 2022? The developments in 2021 provide an interesting backdrop for the 2022 outlook.

BIG PICTURE

High Level 2022 Market Comments:

The Wall Street consensus remains bullish and sees more market gains for 2022. But, there is a wider-than-normal range between bullish views and bearish views and there is a growing list of naysayers who see more downside.

Inflation is seen by most as moderating and becoming less problematic. This benign view could change rapidly, however, if inflation rises higher or persists longer than expected.

The market expects COVID to go from a pandemic to an endemic that the world learns to live with. This may well be the case, but there is a risk of a variant that is highly transmissible and highly virulent.

Markets have had above-trend growth for over a decade, but inflation has been a surprise and the Federal Reserve has significantly shifted its interest rate policy. The Fed has pivoted from a highly stimulative policy to a tightening policy. This is a major shift from a market tailwind to a headwind and suggests that 2022 could be very different.

Increased retail investor trading is disrupting the market’s traditional institutional structure.

China has unique developing risks including increasing property development defaults and President Xi Jinping’s meddling and control over large Chinese companies.

Investment Portfolio Comments and Recommendations:

Rebalance your portfolio. The big run up in mega-cap stocks in the S&P 500 over the last three years means that portfolios are highly skewed to the largest stocks with the highest valuation levels. Rebalancing back to your strategic investment objective allows the purchase of assets with more attractive valuation levels and prospects for better long-term performance.

Tactically overweight U.S. small caps, value style holdings and developed international. Exercise caution on emerging markets due to China.

Fixed Income bond maturity levels should be kept relatively short, with an emphasis on corporate high-quality and high-yield bonds.

Charitable Giving of highly-appreciated stock is particularly attractive given the big stock market gains and high valuation levels. Obviously, there are few opportunities for tax-loss selling, but negative performers should be liquidated to offset capital gains.

Bitcoin/Crypto has had huge gains but this group is still in the speculative stage. Any purchases should not exceed 1-2% of your portfolio. Blockchain investments look like they have broad long-term applications and appear much more attractive than Bitcoin and other cryptocurrency investments.

THE DETAILS

Bitcoin/Crypto and the meme craze were two new large market factors, so special attention is provided directly below. Market Outlook details are provided further down.

2021 High Fliers: Bitcoin and Meme:

Powered by social media forums like WallStreetBets, GameStop, AMC Entertainment and others revolutionized the way markets operate.

Bitcoin, Crypto & Blockchain:

Bitcoin and other cryptocurrency assets performance skyrocketed again in 2021 and drew increasing attention from both retail and institutional investors. Although Bitcoin is the oldest and largest “digital currency”, there are literally thousands of cryptocurrencies and new crypto assets are continuing to be developed.

Bitcoin and other cryptocurrency are essentially a software program run across a network of linked but independent computers. As such, Cryptocurrencies don’t have a physical form but instead exist only as entries in an electronic ledger as virtual or digital money that takes the form of tokens or “coins”. The cryptocurrency ecosystem allows you to trade over independent exchanges (like Binance or CoinBase) or transfer assets by having a new line entered into the electronic ledger that indicates the transfer. In this regard, it is like a bank account statement that shows transfers of digital money. Rather than existing in a physical form (coins, currency, credit cards, etc.), however, they remain entirely intangible. New cryptocurrency is developed by so-called “Miners”, high-powered computer users competing to solve complex cryptographic computational math problems to win the latest block in the blockchain database.

Bitcoin was up 60% in 2021, and up 118% annualized over the last five years. For comparison purposes, the S&P 500 index was up 18.5% annualized over the last 5 years. Bitcoin was also very volatile. Over the last five years, the standard deviation for Bitcoin was 89% compared to 15% for the S&P 500. Although Bitcoin is the oldest and most common cryptocurrency, there are numerous other crypto assets with even higher performance and volatility.

Since the cryptocurrency system exists over a network of independent computers, they are decentralized as opposed to the current centralized financial system. The crypto universe provides an anonymous peer-to-peer electronic currency system that is not controlled by any central authority. Consequently, they can’t be controlled by commercial banks or central banks like the U.S. Federal Reserve. Central banks historically have heavily influenced money supply, interest rates and the value of the dollar. The decentralized mode of operation is referred to as Decentralized Finance or DeFi, a catchall phrase for banking services offered on a blockchain-based platform.

Primary Functions and Benefits:

Store of Value: Bitcoin is a currency store of value like gold, and is sometimes called digital gold. Bitcoin was developed with a limit of 21 million bitcoins that can ever be mined. As of 2021, there have been 19 million Bitcoin that have already been mined, so new mining supply will be limited and it will cease in the future. With Bitcoin supply capped at 21 million, there is a scarcity value that presumably protects against inflation and other risks and these factors helps explain the popularity.

Medium of exchange: Crypto provides an alternative to traditional financial services transactions. Theoretically you could buy a pizza, but high transaction costs make it better suited for the purchase of your next Lamborghini. The industry is evolving, and PayPal’s Venmo app and the Cash App from Block (formerly Square) now make it easy to buy cryptocurrency or to send it to others. Retail shopping outlets can be expected to accept some of the most common cryptocurrencies.

Diversifier: Cryptocurrency theoretically provides portfolio diversification benefits because it is expected to have a low correlation with other financial assets. Crypto has an idiosyncratic risk profile that is different from other fundamental factors. As a result, crypto in a portfolio has the potential to offer a more attractive risk/reward profile.

Convenience and Efficiency: Cryptocurrencies offer innovation, cost reduction and even the extension of financial services to underserved populations compared to the legacy financial services industry. Since transactions occur peer-to-peer, there is a vast swath of “middlemen” and administrative layers that are eliminated.

Primary Negative Factors:

Bitcoin and other crypto assets have No Intrinsic Value: They exist as digits in a computer program and don’t generate cash flow like typical stocks and bonds. Traditional examples of assets that don’t generate cash flow include gold, art, baseball cards, classic/exotic cars, beanie babies, etc., but these examples do have a physical presence. Digital assets are seen by some as evolving as a new, separate asset class that generates returns as the price keeps increasing. Critics derisively say that investment gains are based on the Greater Fool Theory (where you need to find a Greater Fool who is willing to pay even more.)

Regulation: Regulation is a huge, complex, multi-faceted issue. The Securities and Exchange Commission, the Department of Treasury, the Federal Reserve, state banking commissions and regulatory authorities across the globe are all considering regulation related to cryptocurrency. A primary objective is to protect investors in a way similar to current investor protections. There is also a major concern related to systemic risk. For example, coordinated central bank intervention was critical for stabilizing the global economy during the Great Financial Crisis and recession in 2008/2009. If cryptocurrency had been part of the global financial structure during that crisis, it is difficult to comprehend how central banks would have functioned. Meanwhile, as regulatory issues are being deliberated, digital currency benefits are being explored by the Federal Reserve and by other countries. Although most countries are considering digital currencies, China has banned Bitcoin and other crypto-related activities.

Volatility: Price movements of +/- 10% in a day have occurred in the past. As mentioned above, traditional measures of risk like standard deviation show risk many times greater than traditional stocks and funds.

Energy consumption: Crypto creation and transactions require immense electricity utilization to power the decentralized computers. Bitcoin’s annual electricity usage is described as nearly equal to Sweden’s. It should be noted that some cryptocurrencies are more energy efficient than Bitcoin, and continued efficiencies are expected. Obviously, cryptocurrency has a large carbon footprint at this time.

Illicit payments: Since cryptocurrency transactions are anonymous, it is used for money laundering, ransomware, sex trafficking, terrorist financing and other illicit uses.

Taxes: The IRS Form 1040 currently asks if you received, sold, exchanged or acquired any financial interest in any virtual currency. Your crypto exchange will send you Form 1099-K if you have more than $20,000 proceeds and 200 transactions, and a copy also goes to the IRS. The IRS is obviously concerned about tax avoidance and additional monitoring can be expected for holding crypto in an exchange or digital wallet.

Blockchain is Most Intriguing:

The decentralized aspect of blockchain has given rise to the term Web 3.0. The Web 3.0 characterization foresees a third-generation internet where decentralization makes the web more transparent, and efficient, and unleashes transformational potential for business, finance and governance.

Parallels to the DotCom Bubble?

Cryptocurrency assets like Bitcoin are hailed as the next big thing by true believers. They are also seen as pure hype by others. One analyst described being bullish on Bitcoin because he was bullish on cognitive dissonance. Charlie Munger (Warren Buffet’s partner) says “This era is even crazier than the dot-com era” when most stocks became worthless. Jamie Dimon, CEO of JP Morgan-the nation’s largest bank, has described Bitcoin in the past as worthless. Given the passion and disparate views, it seems helpful to reflect on the DotCom Bubble. Between 1997 and 1999 there were 1,460 IPOs. theGlobe.com was the most noteworthy example of excess. The stock went public at $9 on November 13, 1998, it closed at $63.50 on the first day of trading and by August 2001 it fell below $1 and was delisted. Most IPOs from that era were acquired or merged with other companies or simply ceased to exist. Only 25 reported earnings till 2018 to recover their IPO value according to Shivaram Rajgopal, Professor, Columbia Business School. Today there are very few survivors from that time. (Amazon, Nvidia, Red Hat are prominent survivors). Although there were few survivors, the internet is many orders of magnitude larger today than in 1999.

At this time, it is difficult to foresee the long-term prospects for Bitcoin and a raft of other cryptocurrencies. Newer entrants are emerging with protocols that process more transactions at a faster rate and at a lower cost. The industry continues to develop new products, including stablecoins and Non-Fungible Tokens-NFTs, etc. In any event, the blockchain technology appears to have particularly good growth prospects as the internet evolves. This overview is barely scratching the surface, but the impact from innovation appears huge. Although this space is expected to grow to immense proportions, it looks too early to pick the winners and to be confident you have found the next Amazon.

Retail & Meme:

Retail investors became a new market force that drove the meme stock phenomenon. Meme stock traders use message boards like Reddit’s WallStreetBets, Twitter and other social-media platforms to quickly communicate an investment idea, trend or theme. These meme tactics are in contrast to traditional institutional “fundamental” analysis that is based on company financials and valuation. GameStop-GME, a bricks and mortar video game retailer with declining sales, became the first big meme stock. GameStop traded at under $19 at beginning of the year, but hit an all-time-high of $483 by Jan 28, a 25-fold increase. It ended the year at $148. In January, GameStop benefited from a short squeeze on hedge funds and other institutional investors who were “short” the stock. (A short squeeze occurs when investors utilize an option to sell a security now, with the obligation to buy it at some point in the future. The intent is to be able to buy the stock in the future at a lower price. When a stock price rises instead of falls, the short investors end up buying at higher prices, causing a loss on the option trade.)

Social media platforms allowed retail investors to quickly move together and run in packs to pile on to amplify price moves. This “Stick it to ‘em.” attitude against the big guys caused a short squeeze that inflicted massive hedge fund losses. GameStop investors were encouraged to HOLD FOREVER (or at least for the long-term despite short-term volatility), but an online typo, now immortalized as HODL came to be characterized as “hold on for dear life.”

Social media proved to be effective, and the meme stock traders used the same tactic on AMC Entertainment and others. It needs to be said that once the meme stock phenomenon gained traction, institutional traders and others joined the fray trading on both up and down momentum and various other trend following and quant algorithms.

Since meme stocks usually trade on various non-traditional themes, they typically trade at prices well above what would be justified by traditional valuation metrics. As a result, they require investors to “Hold Forever.” Because these investors can’t cause the stock prices levitate forever, they are ultimately exposed to incurring heavy losses. Meme stocks need to recognized as highly speculative and are best suited for short-term traders rather than as long-term investment strategies. Traders must have the capacity to sustain significant losses. Some investors disparagingly comment on YOLO investors as those who’ve never seen a bear market. Nevertheless, meme stock trading has established itself as a major new force in the markets. It looks clear that this trend represents a new generation of investors developing expertise and learning from potential downside, just like every other generation of investors who were educated by losses.

2021 BROADER MARKET PERFORMANCE:

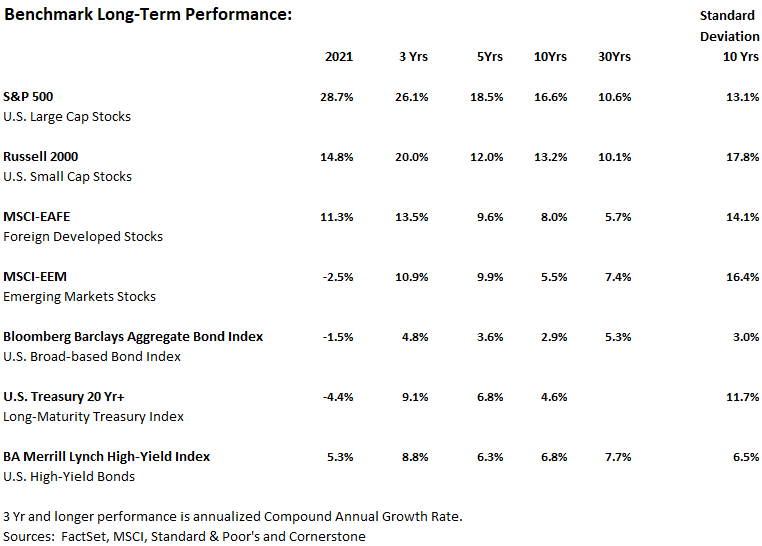

While Bitcoin, Crypto, Blockchain and Meme stocks generated huge gains, the broader market had an exceptional year as well. Going in to 2021, the consensus expectation was for steady gains, but the reality was a big market “melt-up”. Despite supply chain constraints and COVID persistence, the big gains in 2021 helped major indexes generate their best three-year equity performance since 1999. Long maturity bonds did not have a good year, however. The U.S. Treasury 20 Yr+ long-maturity bond index fell by -4.4%, as it was hurt by rising interest rates.

The data from the table above provide context and perspective, especially related to longer-term performance and risk as measured by the standard deviation. As always, recent performance is a poor forecast for the future.

Within the overall market, big cap U.S. stocks, as measured by the S&P 500 index shown in the graph below, maintained their performance leadership and foreign stocks continued to lag. Energy, previously oversold and unloved, was the strongest sector. Investors saw past under-investment in the oil and gas sectors as leading to higher short-term oil prices. Utilities were the weakest sector, but they still managed to gain a very respectable 18%.

Market activity was robust in other parts of the investment universe as well. Investor fervor led to record investments in Initial Public Offerings and SPACs (Special-Purpose Acquisition Companies). Analysis by Bank of America showed that 70% of IPOs for the year through November were unprofitable, a higher level than during the late 1990s tech bubble.

Mergers and Acquisitions deals also set records, with global volume at $5.8 trillion and U.S. volume at $2.5 trillion. Accommodative monetary policy kept interest rates low, and the low rates fueled easy availability of cheap financing and booming stock markets.

Finally, private equity set a record of $990 billion of deals according to Dealogic. Valuation levels are described as more than twice historic levels.

At this time, most everything has been up and to the right. Market momentum appears solid on a near-term basis, but overall growth rates have been well above long-term sustainable levels. Optimism looks overdone and needs to be tempered by sustainable longer-term fundamentals. It is difficult to call the timing of a bear market, but future returns will likely be much lower than the recent past.

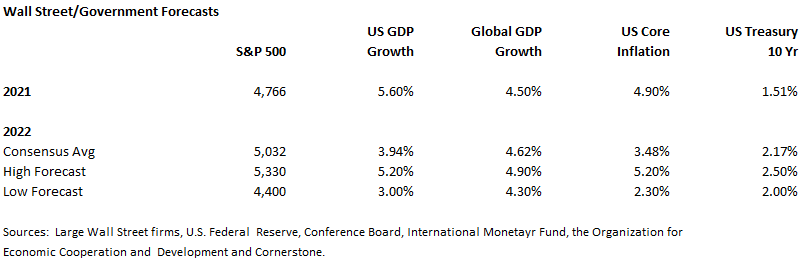

Market Consensus Outlook for 2022:

The table above highlights consensus year-end 2022 expectations for the S&P 500, GDP growth, inflation and the 10 Year U.S. Treasury note. The consensus shows continuing economic recovery, moderating inflation and rising interest rates. Although forecasts are often wide of the mark, the consensus data does reflect what is priced in the market, and it is a helpful starting point for discerning drivers of the markets. An understanding of the consensus expectation also provides perspective as markets react to unanticipated or surprise developments. It is notable that the range between the high and low S&P 500 forecasts are particularly wide, and this indicates heightened risk, uncertainty and volatility. FactSet analysis going back to 2003 shows the consensus typically overestimates year-end market performance, but the consensus has reasonable accuracy most years.

Inflation:

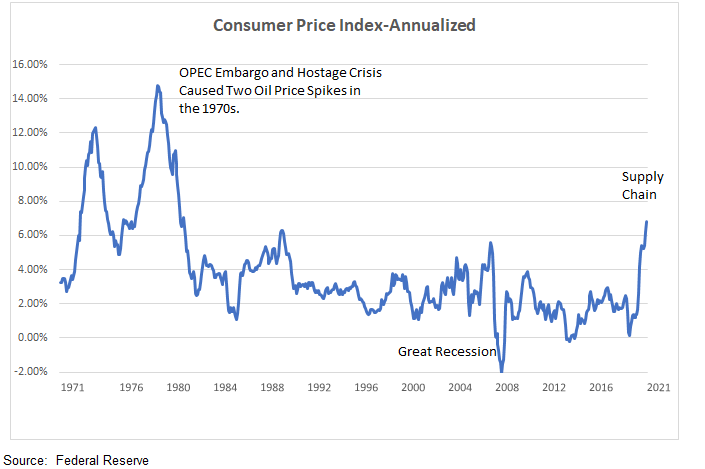

The biggest surprise of 2021 was inflation. The annualized Consumer Price Index inflation rate was 1.4% at year-end 2020, but it rose sharply to 6.8% overall and 4.9% core (net food and energy) during 2021. Increasing inflation began ramping up as the massive container ship Ever Given got stuck sideways in the Suez Canal in March for six days and blocked a key global shipping artery. This event foreshadowed supply chain woes that resulted in an extraordinary surge in global prices, and these constraints aren’t expected to be resolved until well into 2022. Gradually, this “goods” inflation began seeping into the services sector. At this point, inflation has spread into more persistent sectors like wages and rent and there is growing concern related to a wage-price spiral.

The Federal Reserve’s so-called “Dot Plot” forecast shows core inflation dropping to 2.7% by YE 2022 and 2.3% by YE 2023. The Market consensus expectation is higher than the Fed with a 3.5% 2022 inflation rate, and a high-end rate of 5.2% by Wells Fargo. Inflation is clearly running hotter than seen in decades, and the market is currently expecting a gradual moderation in interest rates. History says that moderate inflation rates are not too problematic because inflation allows companies to raise prices and enhance profitability. History also shows that stocks have not been hurt too badly except when inflation is above 6% or when it is negative. Hopefully, inflation will trend down, but vigilance is essential related to the possibility of higher inflation over a longer time period.

Valuation:

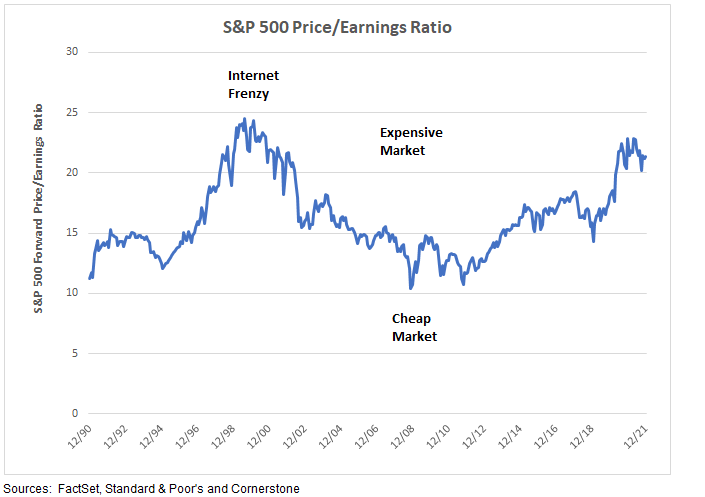

According to most valuation measures, equities have been extremely overvalued for several years. The graph below shows the S&P 500 trading at a relatively expensive forward Price/Earnings ratio of 22. Although the market is quite expensive, at least it is not as expensive as the late 90s internet frenzy. PE ratios do not provide a good market forecast for near-term performance, and history shows that markets can remain overvalued or undervalued for longer than we like or expect. Nevertheless, PE ratios do provide a good indication of longer-term performance. A relatively high PE ratio indicates below-average investment returns over the next 5-10 years.

Small Cap Stocks:

Small cap stocks have outperformed large cap stocks historically, but they have been laggards in recent years. Although small caps are more volatile, they are important in a portfolio’s overall asset allocation plan. Small caps are expected to grow faster than large cap stocks and should provide better performance. Small caps have been under-owned and should benefit from increased investor interest.

Foreign Stocks:

International stocks outperformed in the 1970s, 1980s, and the 2000s, but have trailed the S&P 500 since the 2008/2009 Great Recession. International stocks are cheaper than U.S. stocks, and they are especially cheaper than U.S. large cap growth stocks. They should benefit from investors seeking cheaper valuation levels.

Emerging Market Stocks:

Emerging Mkts: Emerging market stocks are another asset class that has trailed in recent years. Emerging market stocks are more volatile but offer better growth prospects than developed markets based on a younger population and a growing middle class. they are cheaper than developed markets, they offer diversification benefits and they look poised for good longer-term performance.

China is currently a risk to emerging markets because it represents roughly a third of emerging market indexes, and because it has country-specific issues. First, the Evergrande property development company has defaulted on bonds, and additional property development companies are expected to default in the future. Real estate development has been a key Chinese growth driver, but this sector is overbuilt and over-levered, and it will be a drag on future growth. President Xi Jinping has also led a crackdown on technology giants like Ant Group, on private businesses in the education sector and on cryptocurrencies. Xi Jinping is pursuing a common prosperity objective, but he is stifling entrepreneurial innovation. The iShares MSCI EM ex China-EMXC ETF has a Morningstar analyst Gold rating that is a way to invest in emerging markets without Chinese exposure.

BONDS:

Historic Interest Rates:

Interest rates have been trending lower since the early 1980s. The 10-year U.S. Treasury bond interest rate peaked at 15.82% in September 1981 as the U.S. battled double-digit inflation. As inflation subsided, rates have trended lower. Interestingly, forecasters, including the US Federal Reserve, have consistently projected rising rates. Historic long-term bond total return performance has been high due to bond price increases as rates declined. With interest rates at current low levels, there is little potential for additional bond price gains. Instead, any increase in yields will negatively impact bond prices and will be a drag on total return performance. If inflation picks up faster than expected, then longer-maturity bonds will experience significant negative performance.

Interest Rates Since the Pandemic:

The 10-year US Treasury bond began 2021 with a 0.92% yield and ended the year at 1.51%. The rising interest rate environment caused 10-year Treasury Bond price to decline and cause negative total return performance. At this time, real yields (nominal yield net inflation) continue to be negative. Fed policy is to raise short-term rates on securities like the 90-day Treasury Bills, probably starting in mid-year 2022. On the positive side, high-yield corporate bonds generated a 5.3% total return. These high yield bonds have higher yields and shorter maturities that are less impacted by rising interest rates. Looking forward, longer-maturity bonds are expected to face higher interest rates that will further erode their bond price and result in another year of negative total return performance. Since the economy remains strong, high-quality and high-yield corporate bonds again look poised to generate positive returns.

Wrapping Up:

Investment performance has been very strong in recent years, and your IRA, 401k and taxable holdings are likely up significantly. After the huge market decline during the Great Recession a dozen years ago, many pessimistically commented about their “201k” holdings. After a decade of above-average returns and optimism, it might be more realistic to temper optimism by picturing “601k” holdings. Markets will eventually mean revert back to a more fundamentally driven 401k valuation level.

At this stage in the investment cycle, overconfidence is probably the biggest risk for most investors. It is easy to talk about discipline and a long-term perspective, but it is not easy to implement in either up or down markets. Some pundits say we are in the midst of the “Roaring 20s”, and some warn of another “Lost Decade.” The reality is that no one knows for sure. Market knowledge and experience helps maintain perspective, and it also helps to keep in mind that markets can move farther and longer then expected in both directions. Big portfolio winners are likely overweight and expensive, and should be trimmed. If you want to buy Bitcoin or meme stocks, keep the weight below 2%. As always, a long-term perspective, appropriate Investment Objectives, diversification and rebalancing are more important than chasing last year’s high-flyers.

Jeff Johnson, CFA

January 6, 2022

Cornerstone exists to provide educational investment information with a Christian perspective. Some posts are purely about investments (like this one), but other posts have covered stewardship and charitable giving, core values and ESG, Happiness/Money, etc. This is a unique combination, and Cornerstone continues to evolve. Your comments are always helpful and are appreciated.

For additional investment and financial planning information see my Cornerstone website.

The information provided is for informational and educational purposes and it does not constitute personal investment recommendations or investment advice. Past performance does not guarantee future performance.