Each year brings unique and defining circumstances and 2023 was no exception.

-Artificial Intelligence dominated the investment media narrative,

-The Magnificent 7 defied gravity,

-Taylor Swift proved to be not only a record-breaking entertainer, but an economic juggernaut as well.

The year was certainly more disciplined than the meme-stock mania in 2021 when GameStop shares rose 144% in a single day and the typo “HODL” came to mean Hold on For Dear Life.

2023 was also a welcome relief after 2022 with the sobering panic that evoked flashbacks of the financial crash of 2008.

With the over-hyped 2021 and the dismal 2022 in the rearview mirror, 2023 proved to be an exceptional year as the Fed helped deliver a ‘goldilocks’ background of lower inflation without recession

2023 HIGHLIGHTS:

A year ago, the industry consensus was that inflation was out of control and the US economy was on the brink of recession. After a bruising 2022 when both stocks and bonds delivered the worst overall 60/40 portfolio performance since the Great Financial Crisis, most expectations were for modest gains at best. In reality, the economy proved resilient, as employment remained strong, consumers kept spending and inflation dropped faster than most expected. Despite the most aggressive monetary policy tightening cycle in more than 40 years, Fed Chair Jerome Powell was able to pivot from a ‘higher for Longer’ narrative to commenting about likely rate cuts. For many, 2023 will be remembered for the beginning of the return to “Normalcy.” The year will be remembered for a number of key developments.

Artificial Intelligence: Undoubtedly the biggest market buzzword of 2023 was AI after ChatGPT burst upon the scene with a fervor not witnessed since the internet and dot-com mania. ChatGPT, unveiled on November 30, 2022 by Microsoft-backed OpenAI, became the AI poster child as it claimed the title of the fastest-growing consumer software application ever, amassing a staggering 100 million monthly users within a mere two months of its launch.

By April 2023, Goldman Sachs projected that generative AI could propel global gross domestic product by 7% over the next decade and speculated that approximately two-thirds of U.S. occupations could be partially automated by AI. Elon Musk, always provocative, proclaimed “We will be in an age of abundance.” After ChatGPT exploded into public consciousness, chip designer Nvidia delivered one of the biggest earnings surprises in years, and investors scrambled to get in on the action, driving the stock up 239% in 2023. AI was even showcased by a “Christianity Today” cover story that included eleven pages in their October 2023 edition.

Despite achieving significant milestones, such as passing medical board exams, the bar exam and even writing a screenplay, ChatGPT was also known to generate notable errors, called “hallucinations,” that are described in tech terms as the robot brain fabricating information. AI has also been touted as an existential risk, particularly concerning fake news, political misinformation/disinformation and pornography. Unfortunately, sinister outcomes are only now becoming apparent, and we can expect more that are yet to be imagined.

Some detractors liken AI’s market performance to past phenomena like Cabbage Patch dolls and the internet bubble’s pet rocks, but AI looks to offer the prospect for unprecedented “generational” productivity enhancements. According to Bridgewater Associates, “AI could make a host of previously high-cost items very cheap to provide, such as tailored legal advice, customized software, individualized financial planning, and one-on-one tutoring. The health care sector appears particularly well-suited to benefit from faster drug discovery and diagnoses tailored for individuals. To some, technology that automates the research process has the potential to produce a step change in innovation and productivity to cause explosive growth.

The Magnificent 7: The 2023 S&P 500 stock market index has been characterized as the Magnificent 7 and rather derisively the 493 dwarfs. The so-called “Mag Seven” group is primarily comprised of tech darlings: Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla and Meta. This group’s average gain for 2023 was 111%, and their surge generated nearly two-thirds of the S&P 500 Index’s advance.

This stellar performance was based on strong fundamentals. The Magnificent Seven are on track to post a 39.5% aggregate earnings increase in 2023, compared to a 2.6% decline for the rest of the S&P 500, according to LSEG data. Strong earnings growth is expected to continue again in 2024, although by a lesser amount. The strong performance has driven up the group’s valuation level with their overall average forward price-to-earnings ratio at 33.6 times, compared to the S&P 500 index level at 19.8 times.

With this year’s gains being extraordinarily top heavy, portfolios are more concentrated and less diversified. When just a handful of stocks are responsible for most of the market’s gains, it becomes more vulnerable to a large downturn if a few heavyweights fall. It is worth remembering that the Magnificent Seven finished 2022 down -40%, losing $4.7 trillion in combined market value, whereas the remaining stocks in the S&P 500 dropped -12%. These stocks may continue to outperform on a short-term basis, but it is hard to know when they are at their peak, and rebalancing to restore broad diversification prevails in the long run.

Taylor Swift: Taylor Swift emerged as a one-woman economic phenomenon, as record-breaking concerts sparked a surge in spending by filling stadiums and amping up various sectors like restaurants, airlines, hotels, shops, and even beaded friendship bracelets. Her unparalleled Eras Tour, which commenced in March, was followed by her movie theatre rendition of her concert that beat “Mission: Impossible” and “Indiana Jones” at the U.S. box office. She even added new fans and a new dimension of interest to the National Football League by dating Travis Kelce of the Kansas City Chiefs. Through it all, she not only captured the hearts of young women but resonated with parents and individuals of all ages, earning her a dedicated fanbase known as the “Swifties.”

The tour’s immense success shattered attendance and income records nationwide. Bloomberg Economics attributed a staggering $4.3 billion boost to the U.S. gross domestic product from the first 53 concerts alone. Moreover, Philadelphia Federal Reserve officials commented in the Fed’s “Beige Book” (usually quite dry) that Swift’s Eras Tour generated a rise in economic activity, including a gain in hotel bookings, for the first time since the coronavirus pandemic.

Swift’s commitment to her team was as remarkable as her musical achievements, as she distributed a combined $55 million in bonuses to crew members, including dressers, set movers, sound techs, and backup dancers and truck drivers. In an entertainment industry often tainted by cynicism, Swift stood out as a wholesome and positive role model, inspiring countless young women to navigate the complexities of life with strength and imagination. Her emphasis on hard work, humility, kindness and faith-based values has left an enduring impact, encouraging others to follow suit. Swift’s influence transcends music, shaping a cultural legacy that extends far beyond the confines of the stage. By yearend, Time magazine named Taylor Swift as its 2023 Person of the Year. She truly provided a positive, optimistic lift at a time of worry about inflation and recession.

Inflation:

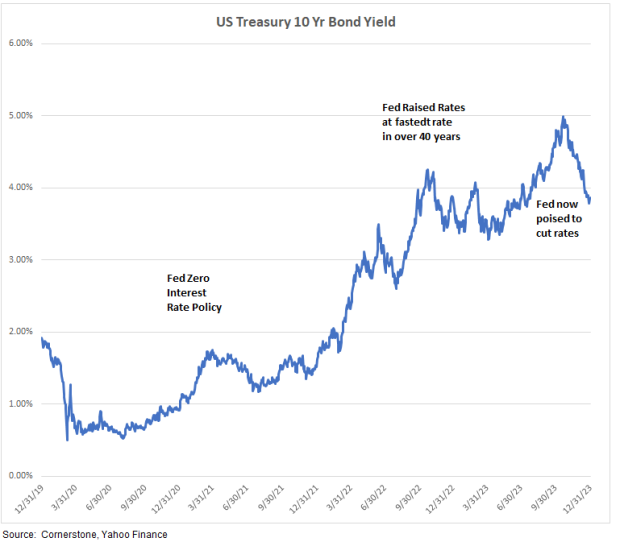

Inflation has certainly been top-of-mind in recent years. After the pandemic, inflation rose on supply-chain dislocations, peaking at the highest level in over 40 years at a 9.1% annualized rate in June 2022. Gas rose over $5/gallon at that time in numerous markets, and this exacerbated the inflationary impact. Although the Federal Reserve first described inflation as “transitory,” they ultimately recognized some of the price pressures were fueled by excessively strong demand. Consequently, they belatedly responded with the most aggressive interest rate increases in four decades. The rate increases, totaling 5%, worked, and inflation is now trending back towards their 2% target. Their objective was to bring inflation down with a “soft landing” that avoided a recession.

Historically, it’s rare to bring inflation down while maintaining a healthy labor market, but so far economic growth remains positive and unemployment hovers near historic lows. Meanwhile, real wages have risen from their pre-pandemic levels so that a typical middle-class American household has higher earnings, more wealth and more purchasing power than before the pandemic. It may be early to declare victory on the inflationary front, but progress thus far is encouraging.

Cryptocurrency: Cryptocurrency remained a major topic throughout the year. Sam Bankman-Fried, former CEO of bankrupt FTX, was convicted of fraud and conspiracy on all seven counts for his role in the collapse of crypto exchange FTX. SBF, as he is known, was found guilty of stealing billions of dollars from customer accounts and of defrauding lenders. A sentencing hearing is scheduled for March 28, 2024 and he faces up to 110 years in prison. US Attorney Damian Williams lauded the jury’s verdict, saying the government has “no patience” for fraud and corruption. “These players like Sam Bankman-Fried might be new, but this kind of fraud, this kind of corruption, is as old as time.” In another case, Binance, operator of the world’s largest cryptocurrency exchange, pleaded guilty and agreed to pay over $4 billion to resolve the Justice Department’s investigation into violations related to money laundering and compliance programs. In addition, Binance’s founder and CEO, Changpeng Zhao, (known as CZ) also pleaded guilty and was forced to resign.

Traditional investment managers describe crypto as having no intrinsic value because it generates no cash flow. Instead it relies on the “greater fool theory” that requires another investor to pay even more than what was originally paid. Current crypto uses include money laundering, illicit weapon sales, drug and sex trafficking, and other criminal activities. Most recently it was used by Iran to funnel funds to Hamas.

Despite the FTX bankruptcy, the Bankman-Fried conviction, and the Binance settlement, crypto had a good year. Bitcoin, although down from a peak of nearly $69,000 in late 2021 gained 155% in 2023 from $16,548 at the beginning of the year to close at $42,182. It is quite volatile, however, with a standard deviation 76.7% compared to 15.2% for S&P 500 index.

Part of the big 2023 price move is explained by the expectation of SEC approval of a “spot” Bitcoin ETF that would allow ordinary investors exposure to actual bitcoin through regular brokerage accounts. Current bitcoin ETFs utilize “futures” and other derivative contracts. There are also “trusts” like Grayscale that often trade at significant discounts to bitcoin. A “spot” ETF would improve price transparency and make trading much easier. This would also increase institutional investor interest. Another factor supporting bitcoin near-term is the “halving” event that is written in bitcoin’s code where payments for so-called miners are cut in half. This keeps a supply cap on bitcoin and supports the price.

Regardless, bitcoin and other cryptocurrency entities trade based on momentum and sentiment rather than fundamentals and they remain highly speculative. For investors considering crypto investing, a 5% weight should be the maximum exposure.

Sector Performance: Technology was the strongest sector (no surprise due to AI) with the SPDR Technology ETF up 55%, and the tech-heavy Nasdaq 100 posting its best return since 1999. The consumer discretionary sector achieved a 38% gain. The SPDR Energy ETF was down -4%, though it was up 64% in 2022. Utilities, the worst sector, were down -10%, and Consumer staples were down -3%.

This wide range of sector performance shows the importance of diversification.

Crude Oil: The price of crude oil fell 11% in 2023 due to record US crude oil production that offset OPEC+ output production cuts. U.S. shale oil production was particularly strong, and the weaker oil price explains the weak oil sector 2023 stock performance. Despite the 2023 price drop, the energy sector is still strongest sector on 3 and 5-year basis.

Gold: The price of gold rose 14% to $2,077 in 2023, and snapped a two-year losing streak. Part of the movement in gold prices relates to actions by central banks across the developed world to lower interest rates, reversing part of their aggressive policy tightening since 2022. Since gold offers no coupon interest, it becomes relatively more attractive as bond yields decline.

Weight Loss Drugs: The health breakthrough of the year was the commercialization of weight loss drugs from Eli Lilly, Novo Nordisk and others. These drugs, technically called Glucagon-Like Peptide-1 (GLP-1), reduce appetite and lower blood sugar. The weight management attributes are clear, but the advantages extend broadly to less diabetes and a host of other related benefits.

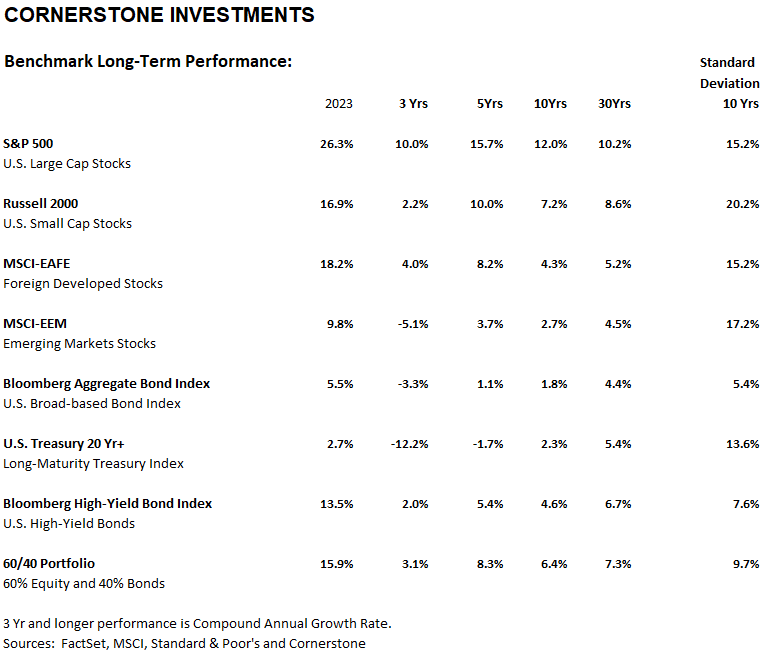

Long-Term Performance and Risk:

The table above shows investment performance and risk going back 30 years. The data shows that the U.S., and especially large-cap assets, have been the strongest performers. Despite the stellar large cap performance, it is noteworthy that large-cap growth and technology stocks were some of the hardest-hit categories in 2022, falling -40%. In reality, the 2023 gains were partially a rebound from 2022. As they went from worst to first from 2022 to 2023, their valuation levels became relatively expensive. Meanwhile, small cap US stocks and international stocks performance lagged but they are relatively cheaper. (more below.)

The long-term stock return is often listed as 10%, and the table shows the 30-year return as 10.2%. It is also interesting that the S&P 500 has achieved a 10.2% average return for total return data going back to 1920.

The bond market recovered from the worst year on record in 2022 as interest rates rose to more normal levels from the Federal Reserve’s previous Zero-Interest-Rate-Policy (ZIRP). The Bloomberg Aggregate Bond index was down -13.1% in 2022, and the Blomberg US Treasury 20 year + index was down -31.1%.

Long-maturity bonds were the weakest performers as investors bailed out of bonds paying low interest rates far into the future. High Yield (junk) bonds performed best as the economy remained stronger than expected.

Finally, the 60/40 diversified equity/bond portfolio staged a strong recovery in 2023. These equity/bond portfolios typically offer a reasonable mix of performance and downside protection. They are typically negatively correlated where strong equity returns are offset by negative bond performance, and vice versa. The unusual combination of large equity declines and historically negative bond returns in 2022 was an anomaly that punished a 60/40 portfolio. Many pundits wrote obituaries for the 60/40 asset allocation structure last year and touted various alternatives, just before a strong 2023 recovery. These marketers proved the folly of short-sighted perspectives.

S&P 500 Large Cap:

The graph above shows the performance for the large cap S&P 500 index starting at year-end 2019 before the pandemic. The S&P 500 large cap index has dominated performance for all major asset classes in recent years and has been helped in large part by the strong performance by the mega-cap Magnificent 7 stocks. Despite the S&P 500 being the leading major asset class in 2023, it has still not topped its all-time high set in January 2022. While performance has been strong of late, the index suffered through the “Lost Decade” in the 2000s, when small caps and other asset classes had far stronger performance. It is clear that strong performance over a decade provides no assurance of similar strong performance over the next decade. The S&P 500 has a concentration of large cap tech/Mag7 and benefits from rebalancing to improve diversification.

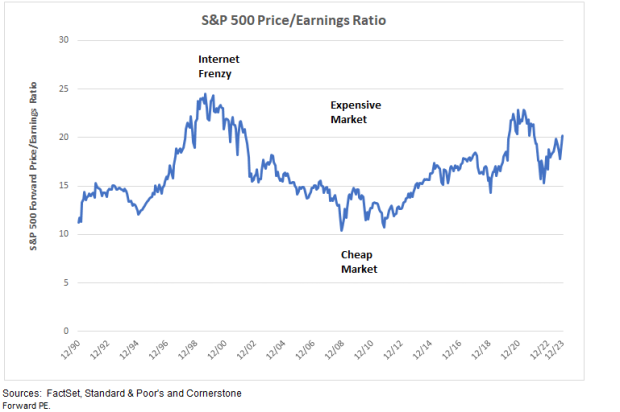

Valuation:

The graph above shows forward valuation for the S&P 500 going back to 1990. The graph shows the S&P 500 index is relatively expensive compared to average levels, though not as expensive as the dot com era from the late 1990s. An analysis by Morningstar shows much cheaper valuation levels for mid and small cap sectors, for the value investment style and for international assets. The relatively high valuation level of the S&P 500 index, gives another reason for rebalancing to improve diversification.

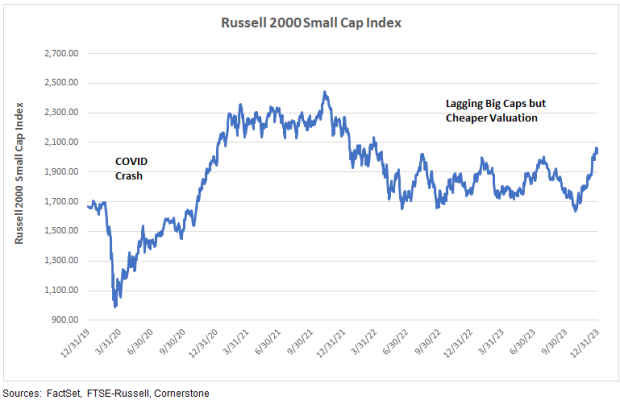

Russell 2000 Small Cap:

Historically, small capitalization stocks have generated higher performance than large caps, but they tend to over/under perform for long periods. Part of the reason for this disparity is that small caps are more sensitive to economic cycles. They can be highly profitable when the economy is strong, but they are more negatively impacted than large caps when the economy weakens. They also tend to have a higher proportion of debt, and the debt is oftentimes floating-rate. Finally, they have less access to capital. In contrast, bigger companies with more opportunities for refinancing were more able to access capital markets to lock in low fixed rates in 2020 and 2021. Small cap stocks should benefit from the current monetary easing and the prospect for a soft landing. Small cap valuation remains very cheap, and this asset class performed strongly in December, and the group looks positioned for additional gains.

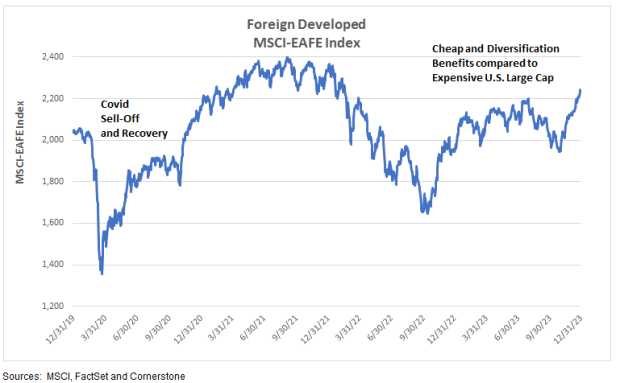

Foreign Developed:

Foreign stocks have been another laggard compared to large cap U.S. stocks in recent years. Part of the reason for this underperformance relates to the appreciation of the U.S. dollar since 2009. According to Morningstar, the US dollar has appreciated 2.2% on an annualized basis over that time period, and that has detracted from foreign performance reported in U.S. dollars. Another reason is the U.S. has been a strong innovator on a global basis, and the U.S. has a much larger tech sector with a faster growth rate.

Investing in foreign markets has provided diversification benefits over time, however. For example, when the S&P 500 declined -18.1% in 2022, the MSCI EAFE index fell -14.5%. Non-U.S. stocks have also led U.S stocks for extended periods, such as the mid-1980s, and from the late 1990 into the mid-2000s. As a result, holding foreign investments should provide better risk/reward performance on a long-term basis.

Emerging Markets:

Emerging market stocks have been another laggard compared to the S&P 500 index. Emerging Markets have trailed due to currency risk, political and regulatory risk, corporate governance issues and higher volatility. Despite the risks, market fundamentals remain favorable. International Monetary Fund data for 2022 shows emerging markets comprise 58.3% of global GDP and 86.1% of global population.

Demographics are favorable with younger populations moving into the middle class and higher spending patterns. Based on this higher growth rate, the October 2023 IMF World Economic Outlook shows 2024 emerging market growth at 4.0%, compared to 1.4% for advanced economies. Emerging markets also offer attractive valuations and diversification benefits.

Emerging Markets ex China:

Another reason for emerging market underperformance relates to the fact that China comprises over 30% of the emerging market indexes, and Chinese markets have performed poorly. Although China’s economic model delivered dramatic growth between 1990 and 2020, it is now struggling to maintain historic growth rates. Looking back in time, per-capita nominal GDP saw a 41-fold growth from $312 in 1980 to nearly $13,000 in 2022, and this lifted hundreds of millions of people out of poverty. The private sector now plays a larger role in the country, contributing to over 60% of GDP according to the Wall Street Journal.

Despite this historic record of growth, recent Chinese investment performance has been negative and major headwinds are expected to negatively impact the future growth rate. Major risks include an unfavorable demographic profile, an unprecedented property slump, low financial transparency, regulatory risk directed at technology, and high volatility. There are also human rights issues and the prospect of a confrontation with China over Taiwan.

High debt levels also weigh on future growth. Much of China’s government borrowing is done by local authorities and some of this debt is off balance sheet. Secular deleveraging is likely to take a number of years. U.S. companies and other Western companies are also reconfiguring their supply chains away from China. Finally, political and diplomatic relationships are at a low level. It was in late January 2023 that an American F22 Raptor shot down a Chinese spy balloon that was drifting across the U.S.

In response to these risks and challenges, major long-time institutional investors and hedge fund investors with long bullish track records of investing in China have changed their perspective, and they are now reducing their Chinese holdings. The amount of money that institutional investors have in Chinese stocks and bonds has declined by more than $31 billion this year, through October, the biggest net outflow since China joined the World Trade Organization in 2001, according to fund flow data.

Given the weak fundamentals and prospects, it is worth considering emerging markets ex China.

The iShares MSCI Emerging Markets ex China Index-EMXC ETF was launched in 2017 and offers an alternative.

Bonds:

The bond market suffered its worst year on record in 2022 as the Federal Reserve rapidly switched from maintaining short-term interest rates near zero, to rapidly escalating rates in response to inflation. As a result, as the Bloomberg Aggregate Bond index fell -13.1%, and the Bloomberg US Treasury 20+ year index fell -31.1%. Long-maturity bonds were the weakest performers as interest rates rose and bond prices fell, causing investors large capital losses. It is worth noting that interest rates are now moving closer to more normal historic levels, and future performance and volatility should be attractive.

Looking to 2024:

One failsafe forecast that occurs towards the end of each year, is that market strategists and economists gaze into their crystal balls and then issue outlooks for the upcoming year. These outlooks are summarized above.

Key points:

-The current consensus for the market shows little upside from year-end 2023. Even the highest outlook (at up 15%) does not reflect heroic assumptions or a repeat of the 2023 investment gains.

-The outlooks mostly reflect an expectation of a soft landing where inflation continues to trend down without causing a recession.

-There is also a theme of a return to “Normalcy” where the Fed is less involved attempting to stimulate the economy with cheap money or restraining it through high rates.

-Commercial Real Estate is seen as the greatest risk as the sector seeks to refinance debt in a higher interest rate environment.

Many investors say it is best to take these outlooks with a grain of salt. Warren Buffett has said that the only value of stock forecasters is to make fortunetellers look good. There can also be a healthy level of hubris and overconfidence embedded in these outlooks. They typically incorporate known risks, but struggle to identify outlier events that can change the direction of markets.

Despite various disparaging comments, there is much value to be gleaned from these outlooks. First, they show the collective perspectives that are priced into the markets by seasoned investors. They also provide a framework for assessing unexpected outcomes that typically occur over the course of a year. While year-ahead outlooks are notoriously off-the-mark in some years (including the big 2023 return), the consensus provides a useful reference point for investment decision making.

It is helpful to remember that the historic average nominal total return for stocks has been around 10%, including dividends and 7% on an inflation-adjusted basis. It is also important to remember that market volatility means short-term investment performance swings widely in both directions and emotion and sentiment often cause worse decisions. Being more informed mitigates against emotion/sentiment. Time in the market is also more important than timing the market.

A good indicator of longer-term future returns is the Cyclically Adjusted Price/Earnings (CAPE) ratio that measures valuation based on real earnings per share over the past 10-years. History shows that a high CAPE ratio (expensive) is correlated with below-average future returns, and a low CAPE ratio (cheap) is correlated with above-average future returns. The CAPE ratio at year-end 2023 is 32.43 and the 30-year average is 27.55 according to JP Morgan. This indicates below average longer-term market returns. This current higher CAPE ratio is no reason to avoid risk, but it cautions against undue optimism.

Longer-Term Opportunities and Risks:

Market outlooks tend to focus on near-term factors impacting the upcoming year, but it is important to consider longer term growth factors and risks. On the positive side, it is essential to keep in mind long-term trends that embed general human ingenuity and creativity into production capabilities and new products. People are also living longer, and are living more productive lives. Moreover, productivity is likely to continue to increase based on new developments like artificial intelligence.

There are clouds on the horizon, however, that could erode future growth rates below the historic 10% equity norm:

Debt in the U.S. and on a global basis has increased significantly since the 2008 Great Financial Crisis and the 2020 pandemic. This increase in debt is particularly true in the U.S., where the total federal debt is now near $34 trillion. The federal budget deficit for fiscal year 2023 came to $1.7 trillion, and the Congressional Budget Office projects generally increasing deficits over the coming years. Federal debt held by the public is projected to rise from 98 percent of GDP in 2023 to 118 percent in 2033—an average increase of 2 percentage points per year. As the debt increases, interest costs have grown as well. The Treasury Department reported that net interest costs reached $659 billion (2.5% of GDP) for fiscal year 2023. Interest is now the fourth-largest government program, behind only Social Security, Medicare, and defense.

In its baseline forecast, the Congressional Budget Office (CBO) projected that interest would cost more than $10 trillion over the next decade and exceed the defense budget by 2027. This trend is widely recognized as unsustainable, but political solutions are not imminent. To fund these increasingly high debt levels, interest rates will need to rise to entice investors. This has the effect of crowding out other investments and causing inflationary pressures.

DeCarbonization-This is a very complex topic, but significant investments will necessary to avoid the worst impacts from climate change. A widely quoted 2022 McKinsey study estimated cumulative spending of $275 trillion globally over the next 30 years on physical assets in energy and land-use to reach net zero. This is well above current investment levels and it provides an indication of the magnitude of these potential investments.

Demographics: Demographics for the developed world show slow growth and an aging population. These dynamics indicate slower economic growth. Fortunately, developing regions provide a partial offset.

What to Do:

Numerous investment comments have been made throughout the various sections of this analysis, but it is important to re-emphasize a few key points:

-Disciplined rebalancing is critical, particularly after large market moves as occurred in 2023. When strong performers have become a larger part of your portfolio, your portfolio becomes more concentrated, less diversified and more adversely impacted once the high-flyers come back down.

-The Cornerstone website provides more information related to rebalancing and other investment and financial planning topics.

-Past performance, especially on a short-term basis, is no predictor of future performance. It is common to become attached to big winners but few provide long-term outperformance.

-Time in the market is more important than timing the market.

-Remember, there are lots of shiny objects, but a disciplined process wins the race.

Cornerstone exists to provide educational investment information with a Christian perspective. Some posts are purely about investments (like this one), but other posts have covered Christianity and Civilization, stewardship and charitable giving, core values and ESG, Happiness/Money, etc. This is a unique combination, and Cornerstone continues to evolve. Your comments are always helpful and are appreciated.

Jeff Johnson, CFA

January 2, 2024

Links for recent posts:

Christianity, Civilization and Capitalism