Tired of earning 0.01% in your checking account and money market fund? For most of the last 10 years higher returns with low risk have been a bridge too far. Well, how about a safe 7.12%? The recent jump in inflation means that the current interest rate on I Bonds issued by the U.S. Treasury has been adjusted upward to 7.12%.

I Bonds are not as exciting as Bitcoin or GameStop, but you will likely sleep better at night.

Overview:

-I Bonds are officially called Series I Savings Bonds, and they offer a guarantee from the U.S. government that you can recover your original investment plus inflation increases based on the Consumer Price Index.

-I Bonds have been available since 1998, and they have offered good inflation-adjusted returns during periods from the 1990s through the mid 2000s. Investment return performance has been weak, however, over the last decade as the inflation rate remained under 2%. In cases where inflation is negative, the return is zero for that period and the principal does not decline. This actually happened in 2009 during the Great Recession when inflation was negative and the I Bond return was 0%. The recent jump in inflation has now made these investments attractive again.

-I Bonds can be considered a very competitive “parking place” for “near cash”, but you can also hold them for up to 30 years.

-I Bonds can be bought up to the last day of any month and the investor still receives the full interest payment for that month.

Inflation Adjustments: The current interest rate for I Bonds is 7.12% (for December 2021 through May 2022), and then it is adjusted every six months based on the inflation rate at that time. My Cornerstone inflation expectation is for a gradual reduction in the inflation rate, and a lower inflation rate translates into a lower I Bond return. Nevertheless, I expect an I Bond investment would significantly beat your bank rate for the next couple years.

Rates are moving up, but … The Federal Reserve announced on Wednesday that they will be raising rates, but don’t expect anything big anytime soon. The Fed’s current “Dot Plot” forecast signals three interest rate increases between June 2022 and the end of next year. The forecast also sees three additional rate increases in 2023 and three more rate increases in 2024. Based on this forecast, short-term interest rates would be around 2.25% by yearend 2024. Although short-term interest rates will slowly rise, these rate increases will rise even more slowly for your deposits in your checking and money market funds. Banks are always very quick to raise rates on loans, but they will delay raising your deposit rates as long as possible. Hey, they are in a competitive business to make a profit and meet shareholder expectations. They have also learned that you will tolerate these low deposit rates because you have had little recourse in the past. It needs to be remembered that your investment portfolio likely holds banks and you will benefit from stronger investment performance.

The maximum annual investment is $10,000 per social security number (plus up to $5,000 more if you elect to receive your federal tax refund in I bonds). If you have kids, you can set up accounts for them as well. So, if funds are available, a married couple could put in a total of $20,000 before the end of 2021 and then another $20,000 in 2022. You could do the same for kids.

You can’t get this from you Adviser/Broker: Although it would be convenient to purchase I Bonds through your existing advisory or brokerage accounts, you need to set up an account with the U.S. Treasury. I Bonds are purchased via the TreasuryDirect.gov website, and it is set up to pull cash from your checking account. There is no charge of any kind at any point. The Treasury website is very intuitive and it is designed to easily walk you through the process.

Liquidity: The I Bonds cannot be liquidated for one year after purchase. They can be redeemed between one and five years but you must forfeit 3 months of accrued interest. After five years they can be liquidated without penalty.

Taxes: You have the option of paying your federal taxes on an annual accrual or you can wait until maturity to pay the whole tax obligation. Like other U.S. Treasury securities, there is no state or local tax. If you use your income tax refund to purchase U.S. savings bonds, complete and file IRS Form 8888 with your tax return. They can also be used without taxation under some conditions for educational expenses.

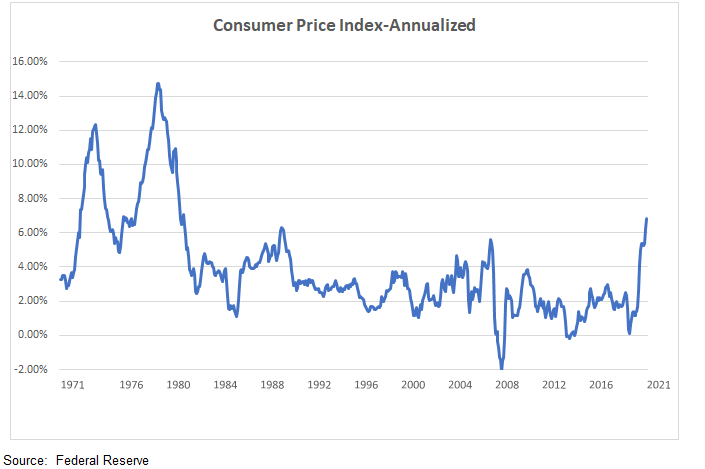

The graph below shows the current upward move in inflation and the history going back to 1971.

Jeff Johnson, CFA

December 18, 2021

Cornerstone exists to provide educational investment information with a Christian perspective. Some posts are purely about investments (like this one), but other posts have covered stewardship and charitable giving, core values and ESG, Happiness/Money, etc. This is a unique combination, and Cornerstone continues to evolve. Your comments are always helpful and are appreciated.